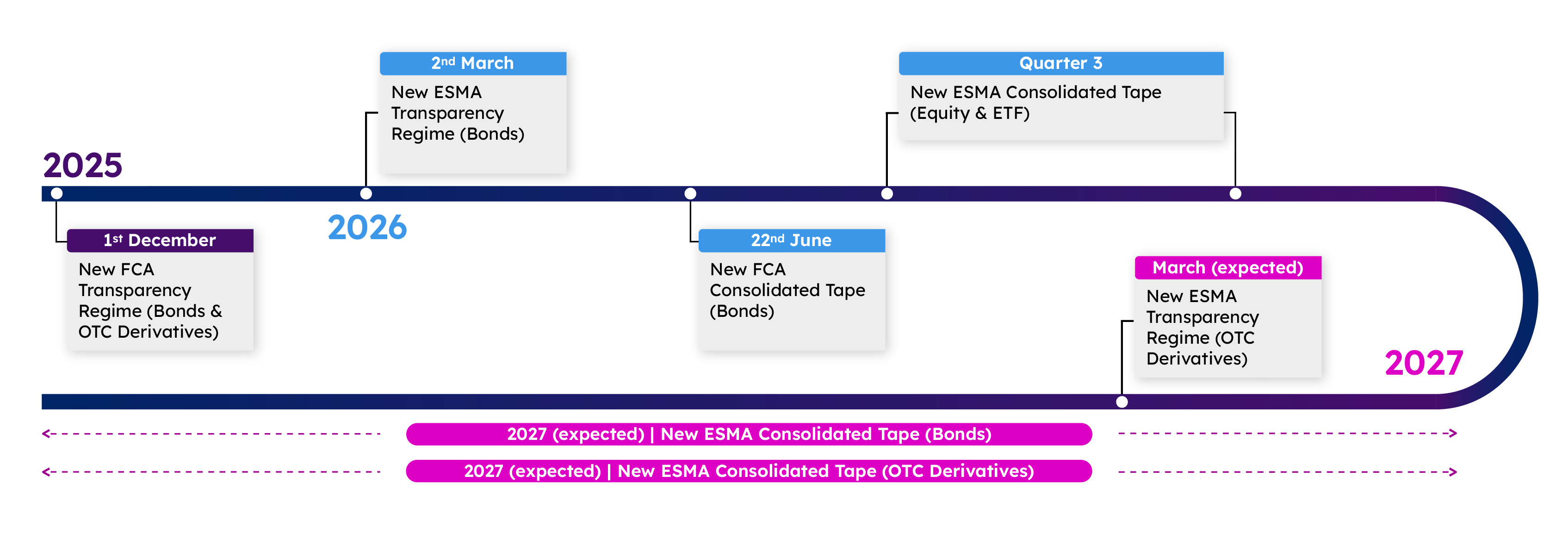

With ESMA’s new transparency regime set to launch on 2 March, attention across the market is increasingly focused on the upcoming changes.

For those who are less familiar with the recent (and upcoming) transparency changes, here is a brief timeline.

So far, the FCA has brought in changes for both bonds and OTC derivatives. As the upcoming ESMA changes only cover debt securities, this analysis will focus solely on bonds.

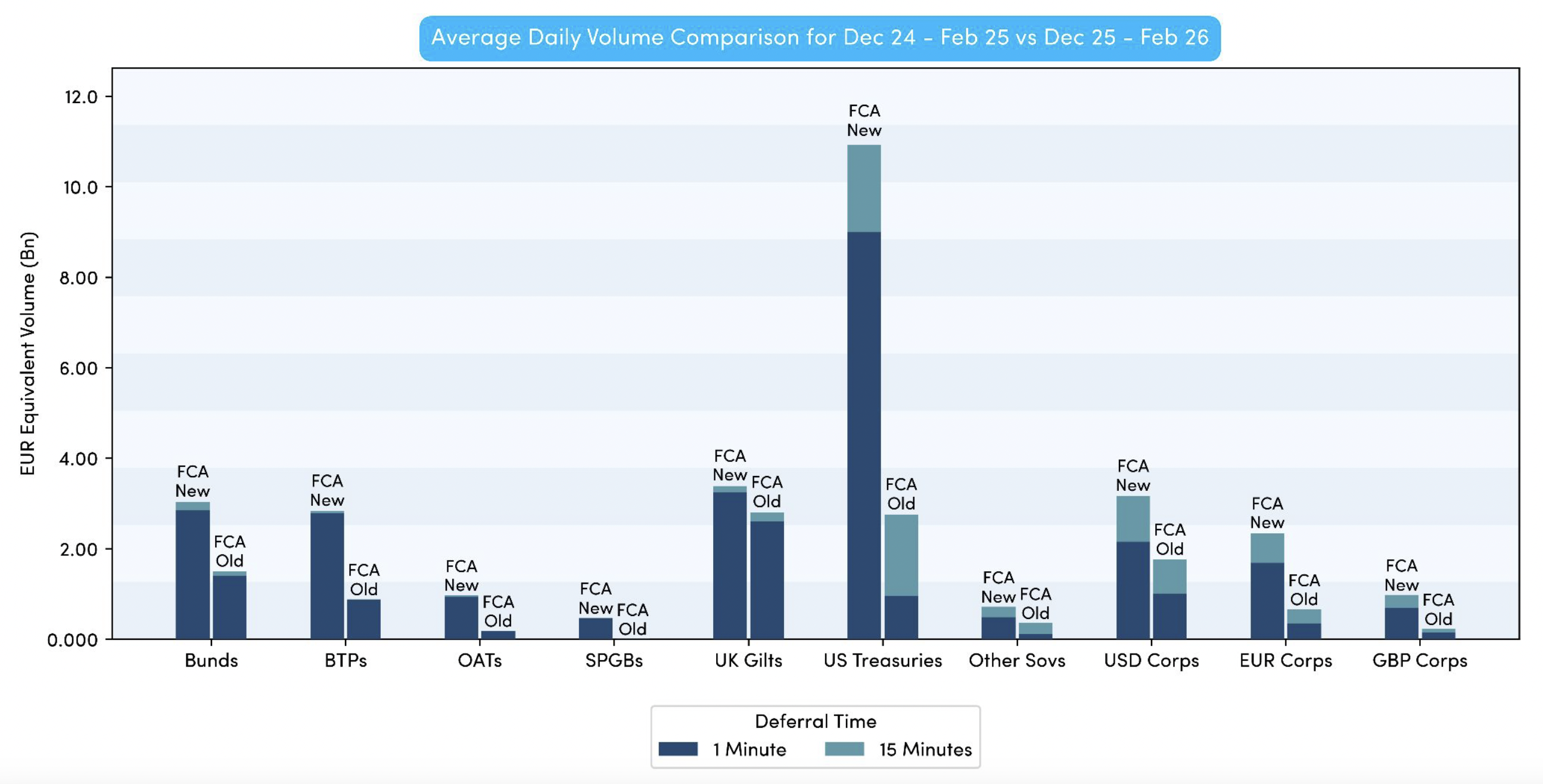

Chart 1 shows the year-on-year change in real-time transparency for bond trades reported to the FCA. The data shows a significant increase across the board (i.e. much higher volumes reported in real time since the changes).

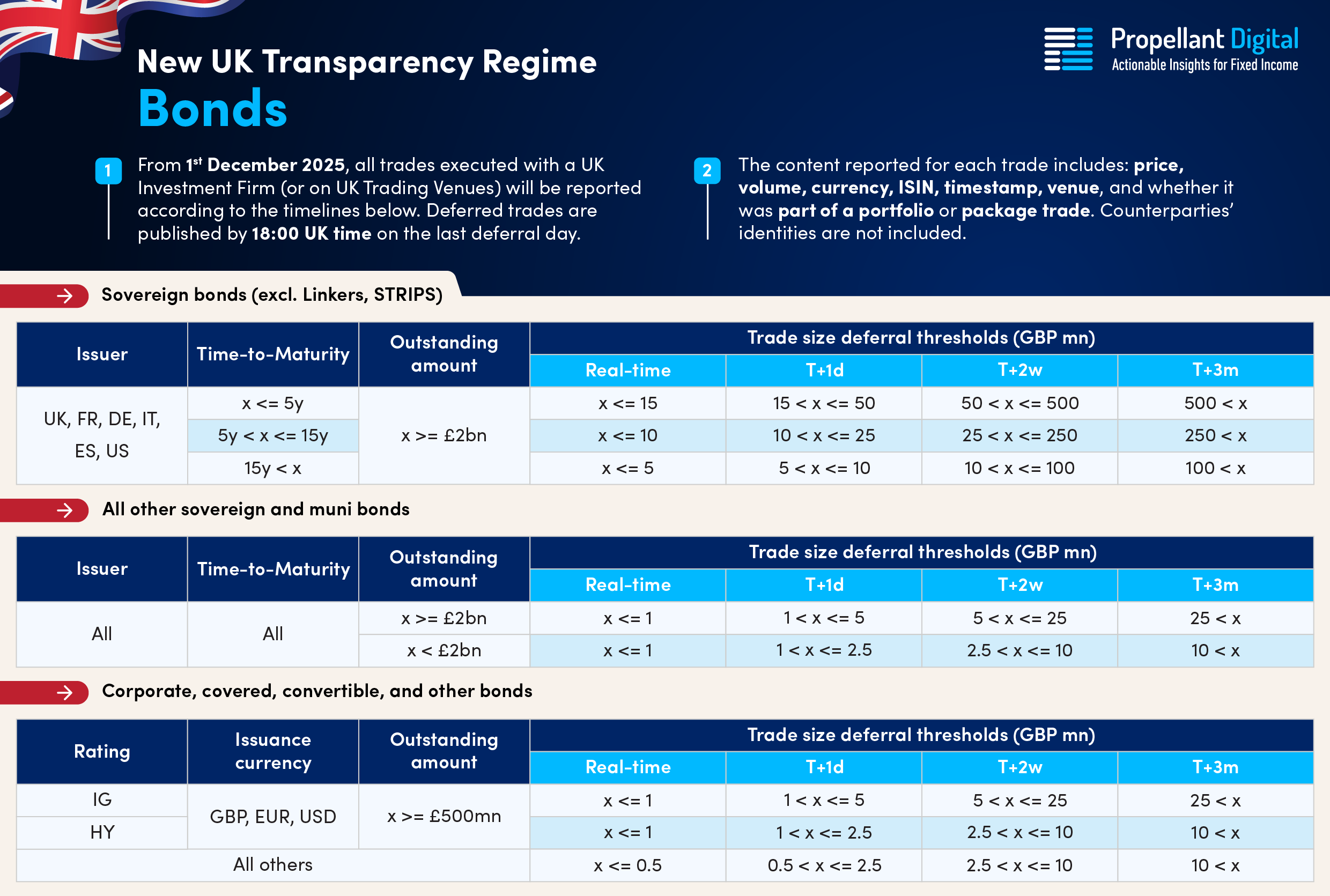

Up until 1 December last year, the deferral rules for trades reported to the FCA and ESMA were the same; however, both regulatory bodies have taken a slightly different approach moving forward. The rules newly implemented by the FCA (i.e. those in effect since December) are shown in Table 1 below.

ESMA and the FCA take differing approaches when it comes to the treatment of Bonds and MiFID trade reporting. The FCA no longer has the notion of ‘liquid’ and ‘illiquid’ (which was previously calculated by the regulators themselves), whereas ESMA will be using outstanding issue size going forward.

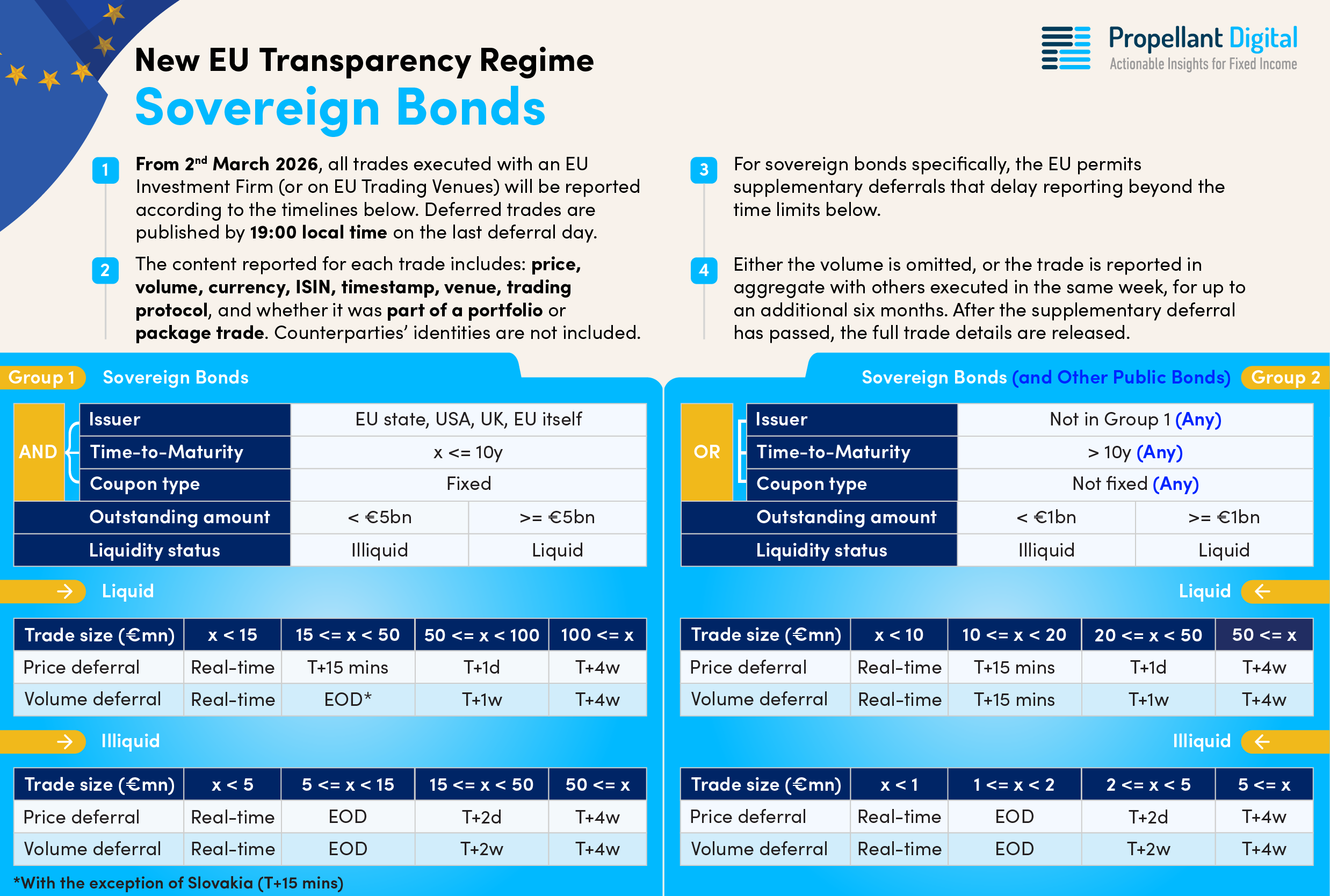

The ESMA deferral rules are split into multiple groups, broadly defined as follows:

One key area of alignment between ESMA and the FCA is the removal of indefinite aggregation and deferral. Previously applied to sovereign bonds, this concept allowed large trades to be grouped together with other similarly sized trades and reported in aggregate on a weekly basis. No transactional level breakdown was ever provided, which could make it challenging for those looking to build models.

This approach has now been retired and a transaction-level breakdown will always be provided. However, there are additional changes within the ESMA regime, we will look into each defined group and outlining its different characteristics.

One final similarity between the two regimes is that both have a real-time category and three deferral categories. However, whilst the FCA consistently uses T+1, T+2 weeks and T+3 months, the ESMA deferrals vary by group (the longest is only ever 4 weeks).

One key difference between ESMA’s group 1 and the FCA equivalent is the scope of sovereign issuers. The FCA only includes six liquid sovereign issuers (The UK, US, Germany, France, Italy and Spain), whereas ESMA includes all EU member states, the European Union legal entity itself, plus the UK and US.

This means far more activity will be captured in ESMA’s group 1. However, it should be noted that this only includes fixed coupon bonds out to 10 years (the FCA has the same stipulation for coupon, but not maturity).

If a bond meets all these criteria, the next assessment is to determine liquidity. If the outstanding amount is greater than or equal to EUR 5 billion equivalent, it is deemed liquid; otherwise, illiquid.

A further important clarification (and only recently confirmed by ESMA) relates to the ability of each National Competent Authority to enforce supplementary deferrals on their own sovereign bonds. The announcement1 clarifies that from 4 May 2026, for sovereign bonds transactions with a size greater than or equal to EUR 15 million and less than 50 million, EU member states will delay the publication of volume until the end of the current trading day. The price will continue to be shown within 15 minutes, and until 4 May 2026, the 15-minute deferral will remain in place for volume (with the exception of Slovakia, which has chosen to keep the 15-minute volume deferral).

If a sovereign (or other public) bond that does not meet the criteria for group 1 falls into group 2 (this will typically capture longer-dated bonds, those with floating coupons and SSA’s). For this category, the liquidity assessment is based on a figure of EUR 1 billion equivalent (as opposed to EUR 5 billion for group 1).

Table 2 below shows the full grid for groups 1 and 2.

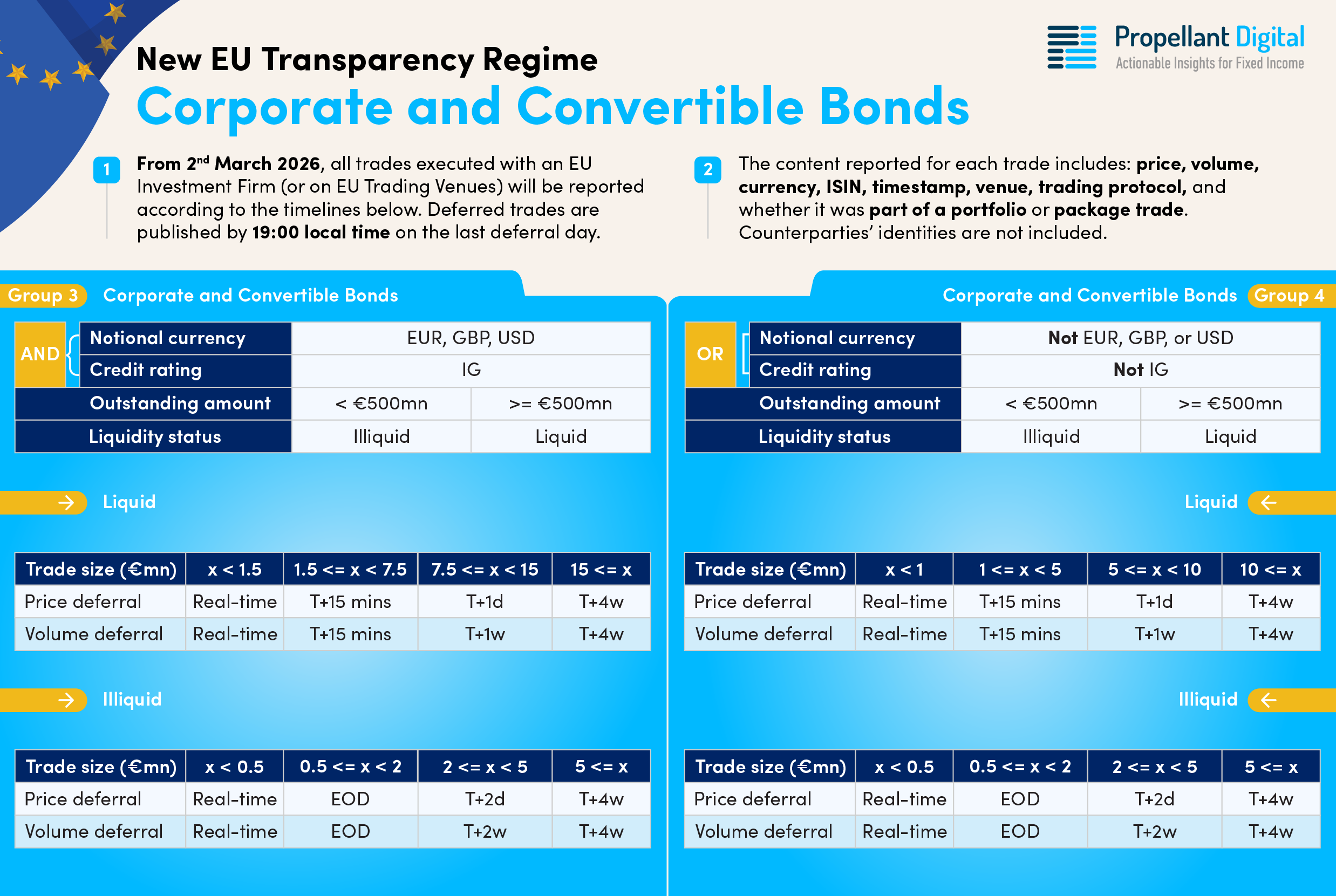

The ESMA groupings can be thought of as a waterfall-like approach, i.e. if a bond does not meet the criteria of a particular group, we can move onto the next one. Following that approach, when a bond does not qualify for groups 1 and 2, it must fit within group 3 or 4 (unless it is a Covered Bond, in which case it will be in group 5).

For group 3, a bond must be denominated in EUR, GBP or USD and must also be Investment Grade (IG) rated. Unlike the FCA, ESMA does not have a specific High Yield (HY) line; instead, all non-IG bonds fall into group 4 (regardless of currency).

If a bond does meet the group 3 criteria, the only additional information required is the issuance size (EUR 500 million equivalent is the liquidity assessment threshold) and then, of course, the trade size.

If a bond falls into the group 4 category, it is neither IG rated nor denominated in EUR, GBP or USD. For example, an AUD IG-rated corporate would fall into this category, as would a EUR HY corporate.

Interestingly, the deferral time frames are actually the same for groups 3 and 4; however, they differ in the trade size required to qualify for a specific deferral. For example, a EUR 7 million trade on a liquid IG (EUR-denominated) corporate would only be deferred for 15 minutes.

If, however, the same bond was downgraded to a sub-IG rating, a similarly sized trade would not have its price reported until the end of the next business day, and the volume would be omitted for a full week.

If it was then tendered and the outstanding amount dropped below EUR 500 million, the trade would then be deferred in full for 4 weeks.

Table 3 shows the full grid for groups 3 and 4.

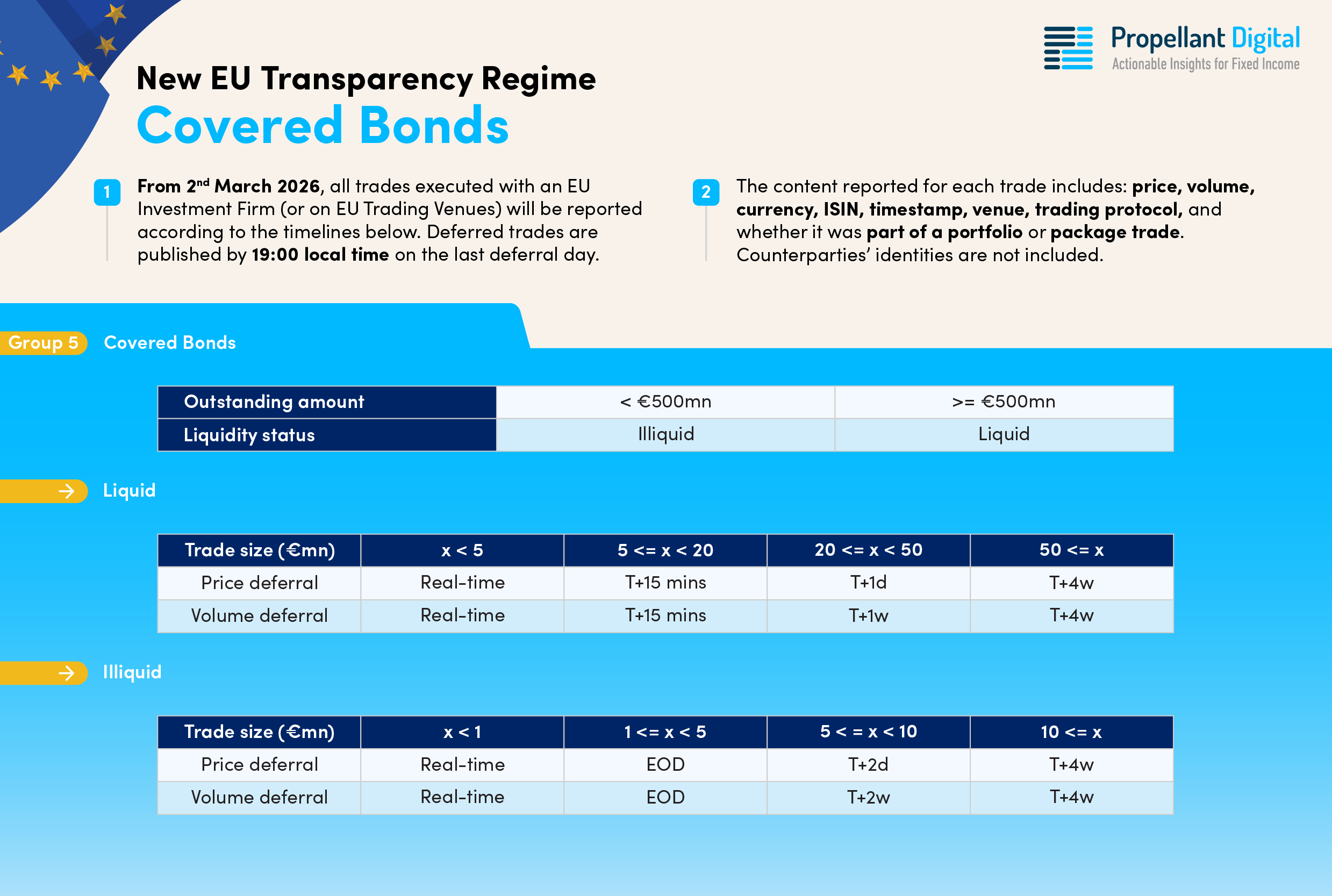

This topic was previously examined in Propellant Insights issue 22 [Read more], where we take a look at Covered Bond activity within Europe and highlight key trends. In this article, we continue the discussion by looking at some of the key differences between how the asset class is treated differently by the two regimes.

It is important to note that the FCA does not have a specific category for Covered Bonds. Instead, these would be captured under the Corporate Bond category, meaning trades larger than GBP 1 million (equivalent) would be deferred for a day or more. Under ESMA, however, the approach differs significantly.

Covered bonds are often EUR-denominated and traded within the EU or EEA; hence, it is logical for ESMA to have a separate category. Additionally, due to the (typically) high credit rating, although Covered Bonds may not trade as actively in the secondary market as some corporates, when they do trade, the lot sizes are typically larger.

The ESMA regime reflects this, with liquid (again, bonds with an outstanding amount of EUR 500 million or more) issues being reported in real-time up to EUR 5 million, and trades up to EUR 20 million only being delayed by 15 minutes. If the bond is deemed to be illiquid, the real-time and 15-minute deferral cut-offs are 1 and 5 million respectively, which mirror the FCA equivalents (on the assumption a Covered Bond will be IG rated).

The full breakdown for group 5, can be seen in Table 4 below.

When this piece goes out, it will be the last trading day of the old ESMA regime; deferred activity for trades undertaken this month will still be reported next week (or later, for corporate bond trades subject to a four-week deferral). However, all new activity from Monday onwards will be subject to the new regime.

Propellant’s team of experts will be on hand to answer any questions and we will be providing regular updates on our observations throughout the initial days. Please get in touch if you would like to find out more.

%20(2).png)