Quite often, when something is eagerly awaited, there is a tendency to feel a bit deflated when it finally arrives. We have been awaiting this week with greater anticipation than most, and we are pleased to say that it has not disappointed!

We are of course referring to the new FCA transparency regime, which went live on Monday 1st December and launched with a bang!

The key changes relate to the thresholds that permit a trade report to be deferred for a specific period of time and the removal of aggregation. In many instances, transactions will be disseminated to the public far more quickly than before. Additionally, trade reports will no longer be bundled; a single report per transaction will always be made available.

Table 1 below shows the updated deferral limits for bonds, which no longer rely on regular liquidity calculations by the regulator, but instead use a clear set of rules based on instrument details such as time to maturity, issuer type, bond grade and outstanding amount.

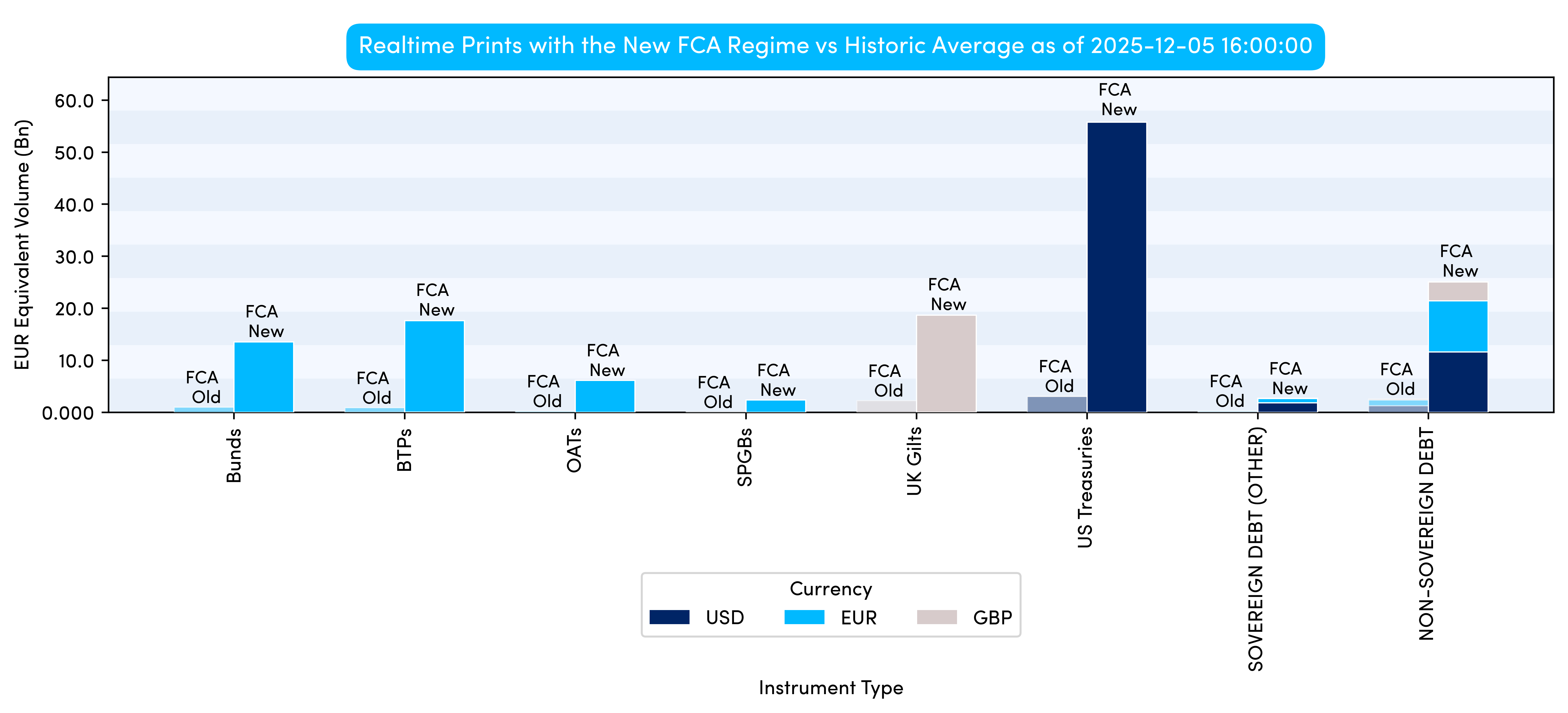

Volumes across the board are up significantly across all types of debt securities, which is not overly surprising given the rule changes. However, one particular point of interest is that under MiFID II, US Treasury transparency is very material. Whilst it is hardly a secret that US Treasuries are the most liquid bonds on the planet, being able to see prints in real-time throughout the day is a new phenomenon.

FINRA’s TRACE (which offers real-time for Corporate and Agency bonds), currently only releases US Treasury activity at the end of the trading day, meaning that the FCA data actually offers greater transparency.

Chart 1 below shows the real-time activity reported in the first week of the new regime, compared to the average (median) reported volumes under the previous set of rules.

The data shows a considerable increase in the amount of flow reported in real-time on sovereign debt, particularly among six issuers classified by the FCA as the most liquid - Germany, France, Italy, Spain, the UK, and the US. However, transparency has expanded beyond sovereign markets, with real-time reported volumes for non-sovereign debt increasing more than tenfold.

The changes do not just impact European (and US) issuers of course; Asia-Pacific, African and Latin American sovereign (and corporate) bonds will also benefit from this enhanced transparency (so long as the transaction takes place on an FCA regulated venue or involves an FCA-regulated counterpart).

Given the explosive start to the FCA regime, all eyes will soon turn to ESMA’s equivalent which begins on 2nd March 2026 and (as with the FCA regime) is expected to result in far more bond transactions reported in real-time.

Whilst the changes to bond transparency attracted most of the focus in the run up to this week, there have also been a number of significant changes to OTC derivative reporting.

Firstly, some of the most interesting (and important) changes are actually not the deferral rules themselves, but the mandatory reporting fields. Both effective and maturity dates are now mandatory, which is likely to be well received across the board and when used in conjunction with the Unique Product Identifier (UPI) can make it far easier to determine the

contract being reported.

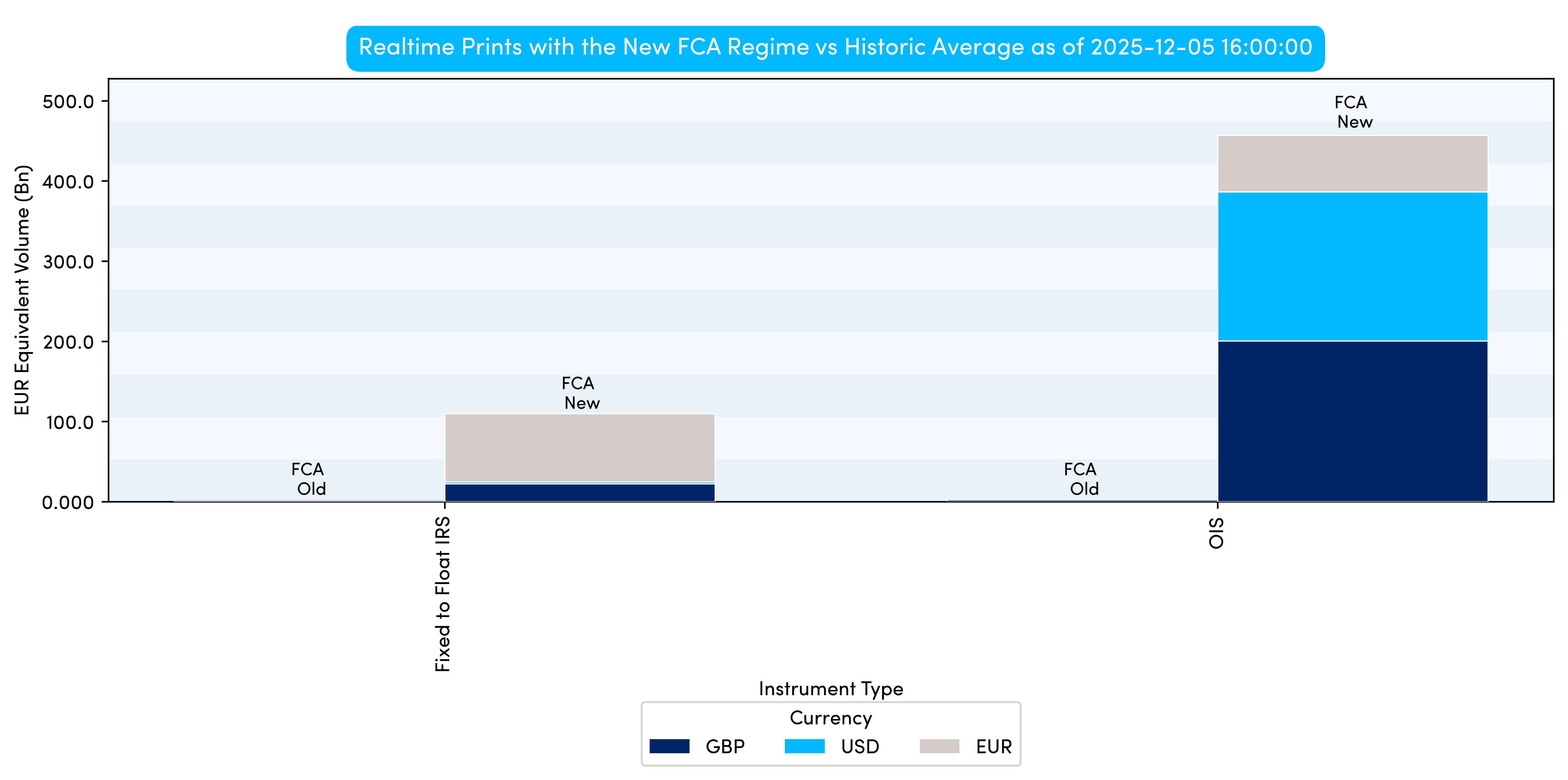

Historically, 89% of EUR IRS notional volumes were reported with a 4 week deferral 1. However, this appears to have dramatically changed since the start of this week, with real-time reported volumes for GBP-, USD- and EUR-denominated IRS dramatically up on the week, as shown in chart 2 below.

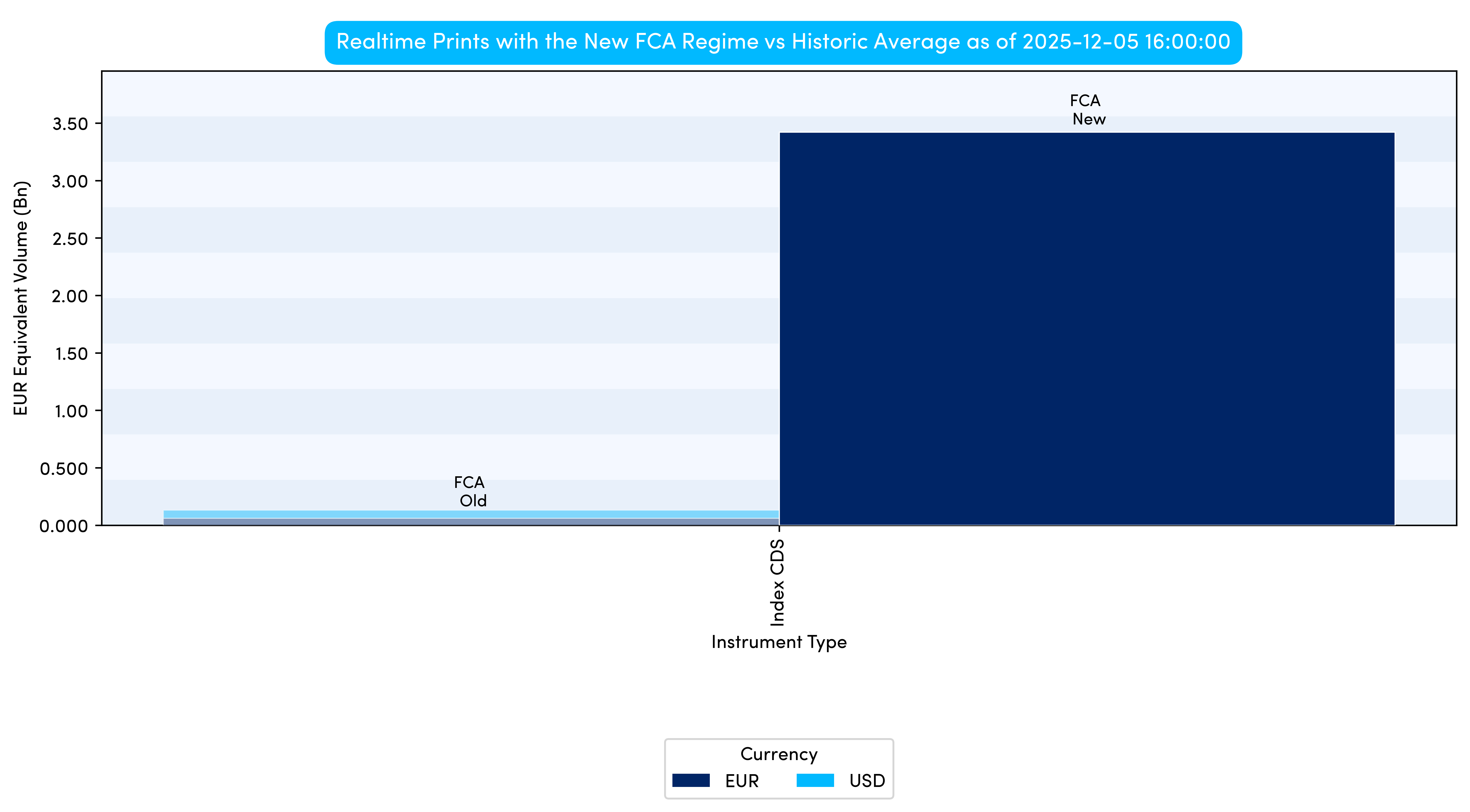

Looking across to chart 3, we turn our attention to Credit Default Swaps. The FCA has importantly mandated the reporting of both the traded spread and the upfront fee, meaning the data is far more usable than ever!

The reporting is focused around only the two most liquid contracts (iTraxx Main & Crossover), however even with the reduced scope, the reduced reporting timelines mean real-time volumes again are up significantly.

The new reporting regime is of course in its infancy, however the early indications suggest that transparency is on the increase. Time will tell if this trend continues, but the initial signs are positive.

It goes without saying that as we enter the new year, the attention will rapidly shift towards Europe and the ESMA equivalent regime.

1https://www.clarusft.com/what-we-need-to-do-to-fix-mifid-ii-data/

%20(5).png)

%20(4).png)