Intraday Transparency in U.S. Treasuries: What UK Reporting Data Shows

.png)

Following the previous article about the US Corporate bonds, Vincent Granjean - Founder & CEO at Propellant Digital, keeps looking at US Treasuries (UST) activity.

---

After looking at US Corporate bonds, I ran the same intraday lens on UST activity reported in the UK under the new regime. I’m not focusing on the headline “% real-time” number, but some more practical points.

Firstly, when does transparency actually show up during the day? Secondly, does it look different if you measure trade count versus notional?

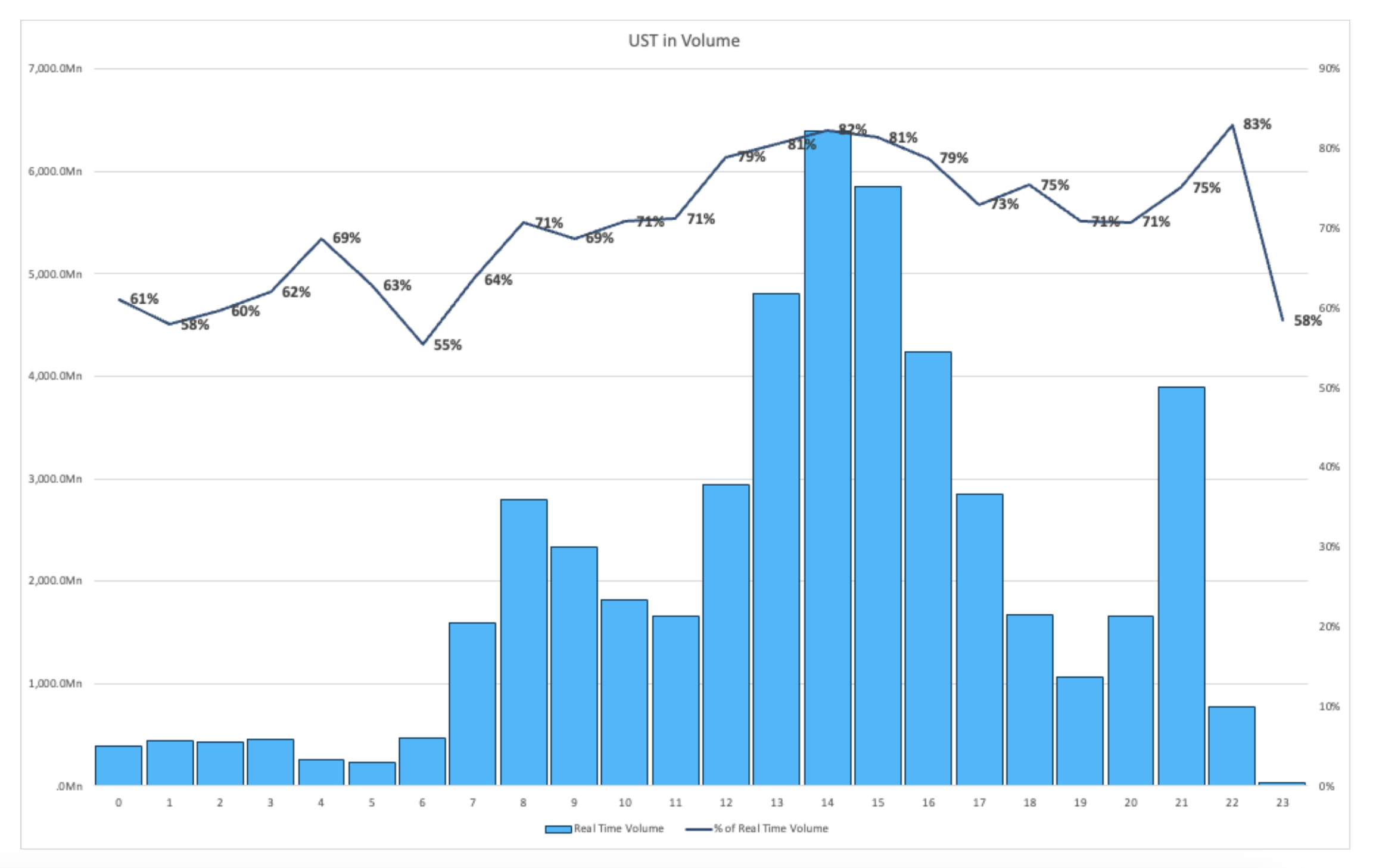

The charts referenced below show UST activity reported in the UK, using average daily intraday volume for January 2026. This is then grouped hourly (for both volume and transaction count) then complemented by a more continuous intraday notional view.

To complement the hourly averages, the chart below shows the same story in a more continuous way. The total notional per minute, split between Real-time and Deferred reporting. I find this view makes it easier to see where activity clusters intraday.

1. Intraday activity is clustered in time with pronounced peaks

UST activity (in this UK-reported dataset) is clearly time-clustered rather than evenly distributed. The continuous notional chart clearly highlights this, illustrating the long quieter stretches and then concentrated periods where activity ramps hard.

If you’re building pricing models, liquidity metrics, or intraday analytics, this matters because assuming a stable “average” market throughout the day can lead to poorly calibrated signals.

2. The transparency picture differs for trade count vs notional

Just like in US credit when asking the question “how transparent is it?” The answer depends on what you measure.

On the notional chart, the real-time share of volume is consistently high across most of the day (and tends to be strongest during the main activity windows). On the trade count chart, the real-time share of transactions is materially lower for much of the day, only improving late.

So you can have a tape that looks very good from a volume visibility perspective, while still being less complete when looking at print-by-print visibility (i.e. a transaction count).

3. A busy tape can still be incomplete

This is the practical takeaway: transparency is subjective.

Count-based transparency tells you how quickly the market becomes visible for breadth (signals, price formation, frequency of prints). Notional-based transparency is more about depth (how much size is actually observable in real time).

If you only look at one of these, it’s easy to draw the wrong conclusion about how observable liquidity in the market really.

4. How this compares to US corporates

Having looked at the same intraday cut for US Corporate bonds, the contrast with USTs is pretty striking.

The real-time share of UST volume stays high through most of the day, especially during the main activity windows. US corporates have a higher proportion of real-time prints than the associated volume. In credit, data becomes visible quickly, when considering the overall number of prints, but the notional picture is much less complete in real time.

So, at a high level, the transparency lens flips: USTs: stronger notional-based visibility than count-based visibility. US corporates: stronger count-based visibility than notional-based visibility.

This is why I think it’s risky to quote a single “% real-time” statistic without saying whether it’s count or volume. The story can look very different depending on the asset class and the lens.

So what?

For me the takeaway is the same: transparency isn’t just “more” or “less.” It has a timing profile, and it behaves differently depending on whether you look at count or notional, especially when deferrals are part of the design.

Curious how others see this: when you think about transparency in rates, do you care more about “how much size becomes visible quickly” or “how quickly the prints show up”?

Important coverage note (what’s included today and what isn’t yet)

This dataset currently captures only trades reported as Real-time, T+1D, and T+2W. Trades in the longest deferral bucket (T+3M) won’t start being observable until March 2026. As with the credit analysis, we wouldn’t expect T+3M to materially change the transaction count picture, but it could still matter for interpreting the non-real-time volume portion once it becomes visible.

.png)

.png)

.png)