When looking at MiFID data, a common misconception is that only trades on European issuers are reported. In reality, the spectrum of issuers is truly global, so long as one entity involved in the trade falls under ESMA or FCA jurisdiction, it is reportable. This means that not only is MiFID data the most complete source for trade prints on EUR- or GBP-denominated corporate and sovereign bonds, but it also contains a vast amount of activity in Emerging Market debt.

Whilst Emerging Markets can be a broad term, this analysis specifically focuses on sovereign-issued debt across the Americas.

Firstly, we can break up the Americas into North and South using ISO/UN classifications.

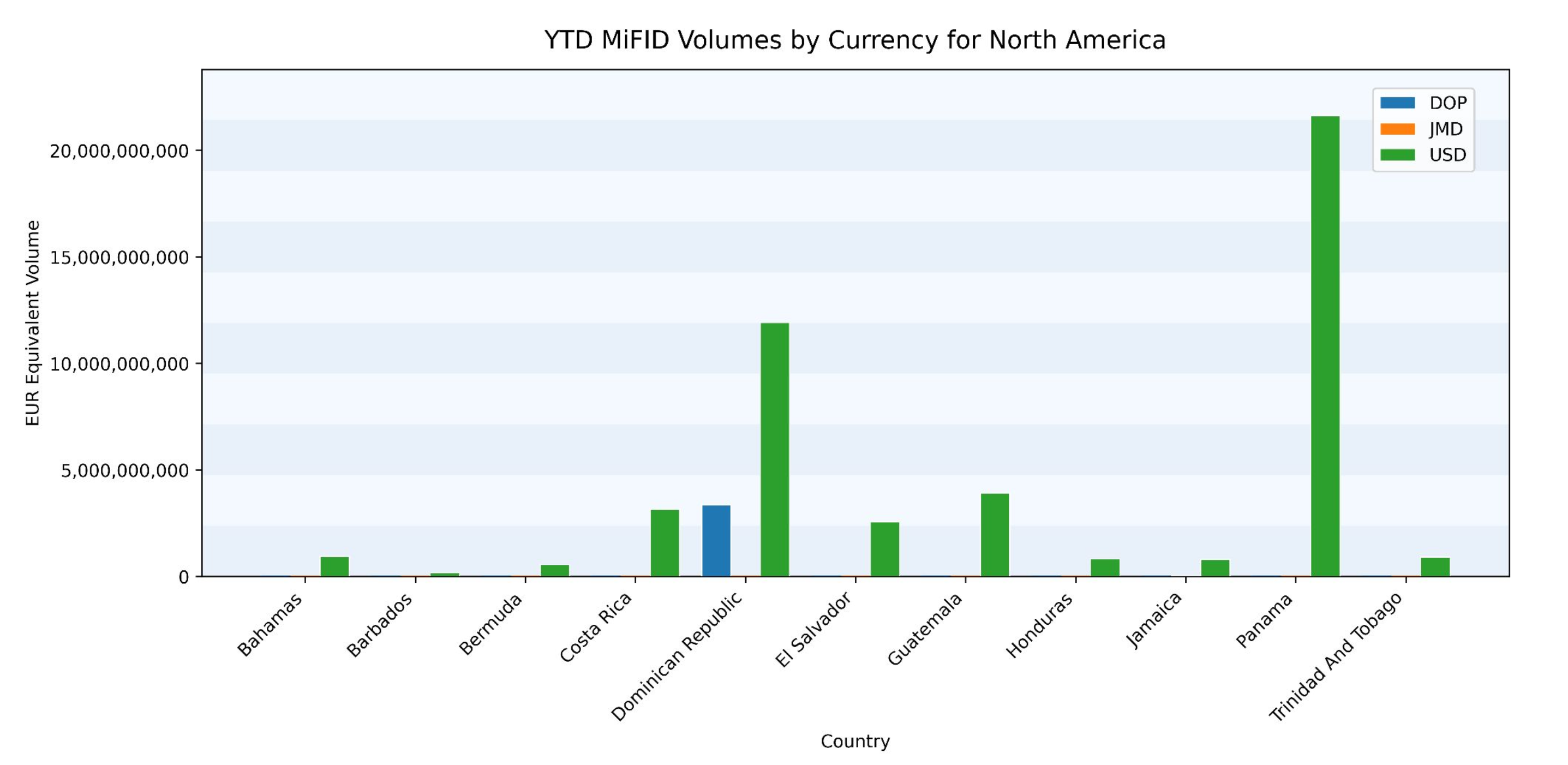

Starting with North America (even excluding the U.S., Canada and Mexico), we can see the bulk of activity is in USD, with a very small amount in Dominican pesos, which highlights the diversity of currencies available in the MiFID data.

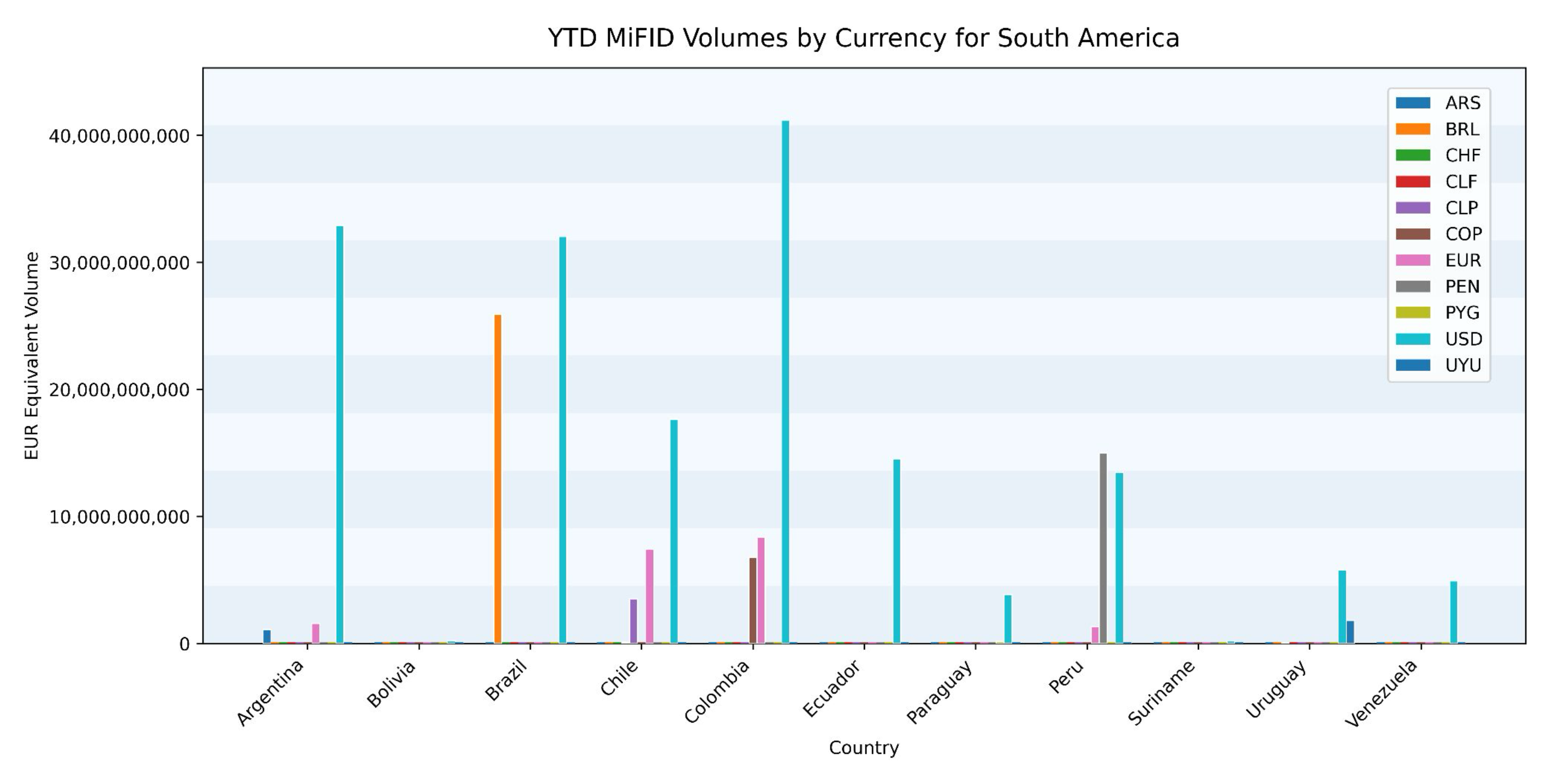

Moving onto South America, things immediately get a lot more interesting. Chart 2 below shows that whilst USD is still the largest currency by volume, significant flows are also reported in local currencies.

The volumes shown in chart 2 are all EUR equivalent, so it is interesting to note that activity reported in Brazilian real-denominated debt is approaching the USD volume. Along similar lines, but perhaps more surprising is that Peruvian Sol debt actually reports more YTD flow than USD-denominated government debt.

Multiple South American governments have outstanding EUR-denominated debt, therefore it is not unexpected to see activity on multiple sovereign credits. Whilst it's highly likely a significant proportion of LATAM secondary market activity is not reported under MiFID, the data we have looked at clearly highlights that there can be significant value in using the data to unlock transparency in an otherwise opaque market.

%20(5).png)

%20(4).png)