.png)

With the recent introduction of the new transparency regimes, an interesting (and perhaps overlooked) trend has emerged: the inconsistent reporting of category 2 instruments.

ESMA takes a slightly different approach, there is no notion of a ‘Category 2’. However, there are different deferrals for the instruments that correspond to those in the FCA’s Category 2. We will look at ESMA’s treatment of the same group of instruments.

ESMA does not have a ‘Category 2’, instead outlining the deferral treatment for each of the corresponding instrument types:

There is no equivalent to the FCA’s ‘Derivatives Traded on Trading Venues which are not Category 1’ as ESMA clearly defines2 the scope of MiFID reporting for OTC derivatives to cover only:

This highlights striking differences between the two regimes, particularly for Fixed Income instruments. Therefore, we will now look more closely at the implications for Structured Finance Products and Exchange Traded Notes.

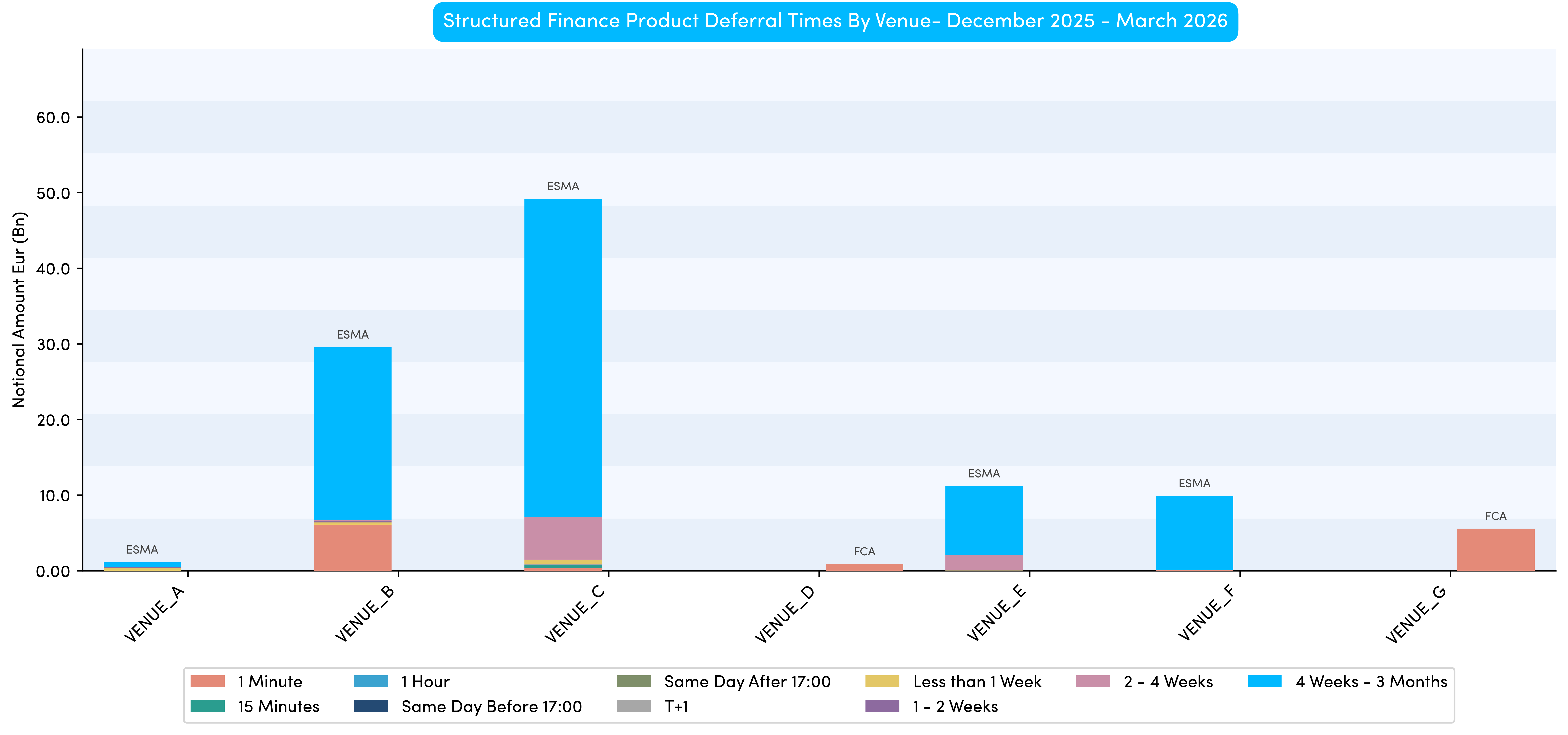

Structured Financial Products (SFPS) have a distinct deferral regime, which may have passed under the radar or been cast aside as seemingly inconsequential (to flow desks in particular). However, what is captured under the SFPS definition can be notable, with active issues such as AWLN 6.625 1/15/29 receiving differing deferral treatment not only across different regimes, but also by different venues.

Chart 1 below shows a large variance between venues, with some reporting in real-time and others with significant delays.

Whilst Chart 1 presents an interesting picture, the true impact of the differing treatment is not immediately obvious. For example, a lot more volume trades on ESMA venues, where the deferral length is often longer than four weeks. In contrast, at least two FCA venues appear to be reporting activity in a much shorter space of time.

Given the timeframe under consideration (December 2025 to March 2026), it is reasonable to assume that most ESMA volume captured above would have been reported under the old regime. As such, we may not want to put too much weight on the historic ESMA volumes (under the new ESMA rules, the price is deferred by two days and the volume for two weeks).

The FCA activity is of more interest as the venues themselves decide the deferral period (rather than the regulator) resulting in a divergence between the venues. Chart 2 illustrates the impact of this, using a single security (AWLN 6.625 1/15/29).

By considering a single security, the aforementioned divergence becomes much more apparent. Venues A and E report in near real-time, Venue’s B and D report between four weeks and three months and Venue C reports between three and six months.

.png)

The above breakdown is something that could have an impact on trading decisions as it is fair to assume that up until now, venue selection may not have considered venue deferral policy (instead focusing on direct economics). However now, for some asset classes, it may be impossible to ignore.

A similar pattern can be see in Exchange Traded Notes (ETNs), with some (FCA) venues reporting in real-time and others (mainly ESMA) reporting much later. This further reiterates the point that venue selection matters even more than ever.

%20(5).png)

%20(4).png)