If you are an Emerging Markets (EM) trader, or perhaps just wanted to ease into the new year, then the events earlier this week may have come as a bit of a shock!

The US undertook military action against Venezuela on the morning of 3 January 20261 and inevitably this has far wider repercussions.

On the morning of Saturday, 3 January 2026, the US launched an operation to capture Venezuelan leader Nicolás Maduro and his wife, Cilia Flores. Both were apprehended and transferred to the US to face drug trafficking charges.2

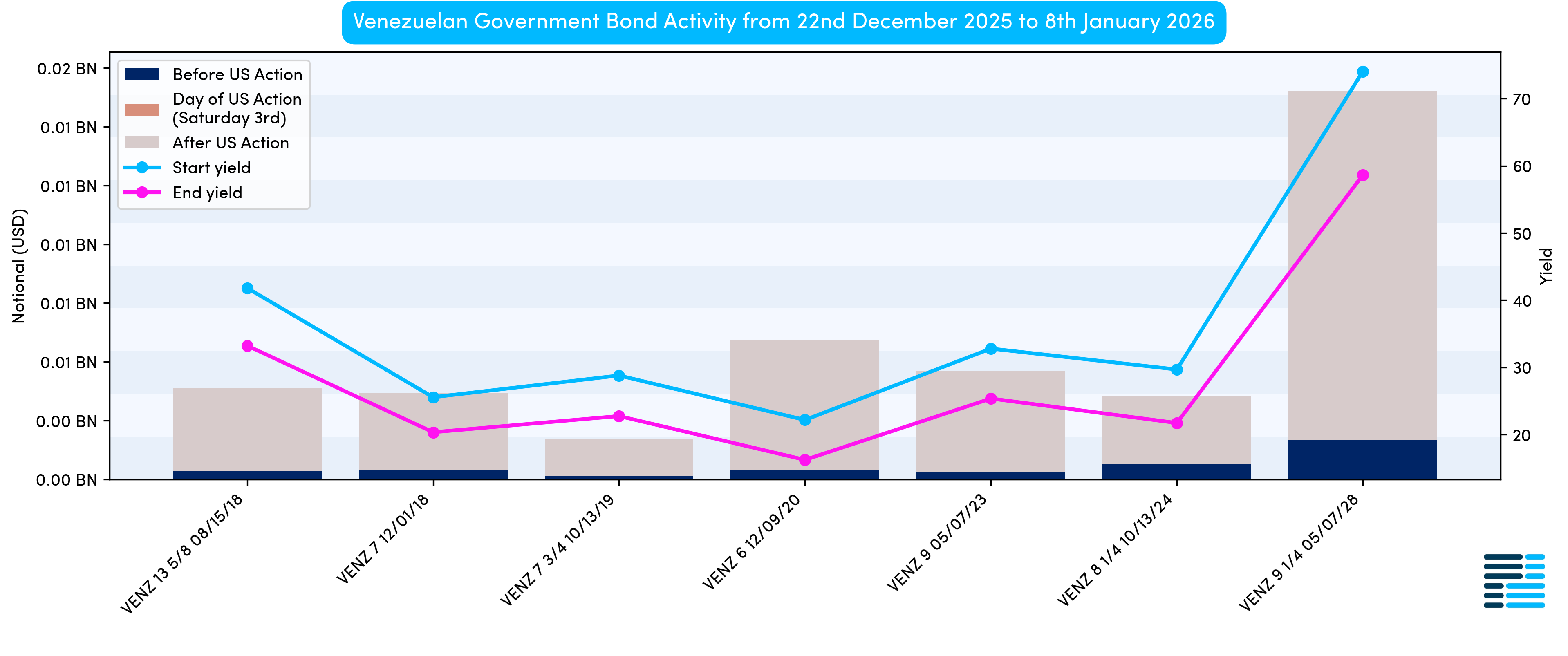

It is too early to say what the long-term impact domestically will be; however, courtesy of MiFID, we can see what the bond markets think, as shown in Chart 1 below.

Above, we consider USD-denominated debt issued by Venezuela and can immediately see that yields have tightened quite significantly across the board. We also note more activity in the first few days of January, than the end of December (albeit, we cannot read too much into this, given the holiday period).

It is important to note that most Venezuelan bonds are still outstanding, having not been repaid on the original maturity dates. Only the 9% 2028 issue above has not exceeded its original maturity date. Additionally, coupon payments have not been made (in some cases) since 2017.

Above, we consider USD-denominated debt issued by Venezuela and can immediately see that yields have tightened quite significantly across the board. We also note more activity in the first few days of January, than the end of December (albeit, we cannot read too much into this, given the holiday period).

It is important to note that most Venezuelan bonds are still outstanding, having not been repaid on the original maturity dates. Only the 9% 2028 issue above has not exceeded its original maturity date. Additionally, coupon payments have not been made (in some cases) since 2017.

After the events, President Trump updated the media and made comments alluding to potential action against three other countries in the region: Cuba, Colombia and Mexico.4

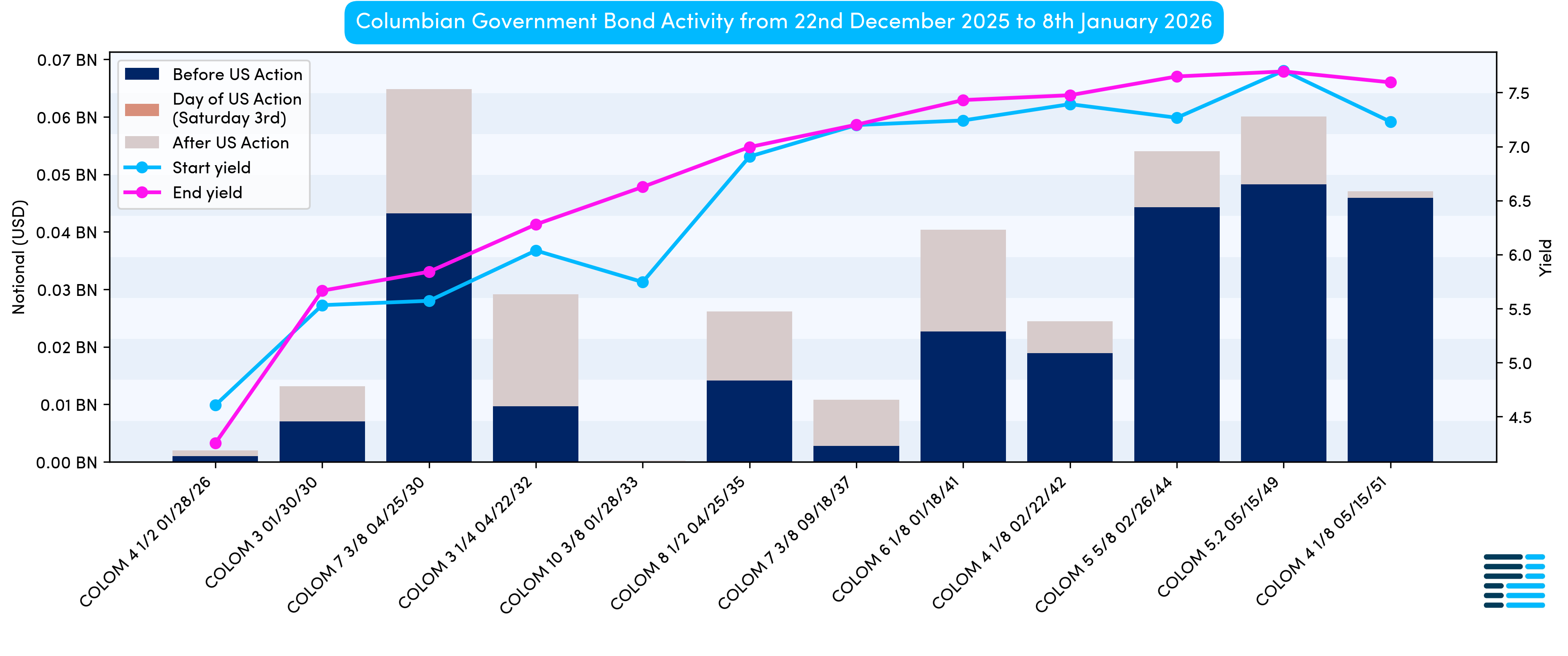

Cuba does not have debt transactions reported under MiFID during the period. However, Chart 2 below focuses on the Colombian Government bond curve (again only USD-international issues, rather than COP-denominated domestic issues).

Chart 2 illustrates that the Colombian curve shifted marginally upwards (i.e. yields widened). This outcome is not illogical, given the country was referenced in Trump’s speech4. What is interesting, however, is that despite this widening, volumes reported appear far lower than those reported in the last week and a half in December.

This can be partially explained as aggregation and deferrals still exist under the ESMA regime. Whilst aggregation no longer exists for trades reported to the FCA, deferrals are still applicable for larger trades (hence, we will need to wait and see if additional volume is reported in due course).

Another country mentioned by the US (not quite in the same fashion as the others), is Greenland (which of course is part of the Kingdom of Denmark5). As reported on 4 January, President Trump stated6: “We need Greenland from the standpoint of national security”.

Greenland does not typically issue sovereign debt (at least not in the public markets). Therefore, no activity was reported under MiFID, making it difficult to quantify any impact of such statements from a bond market perspective.

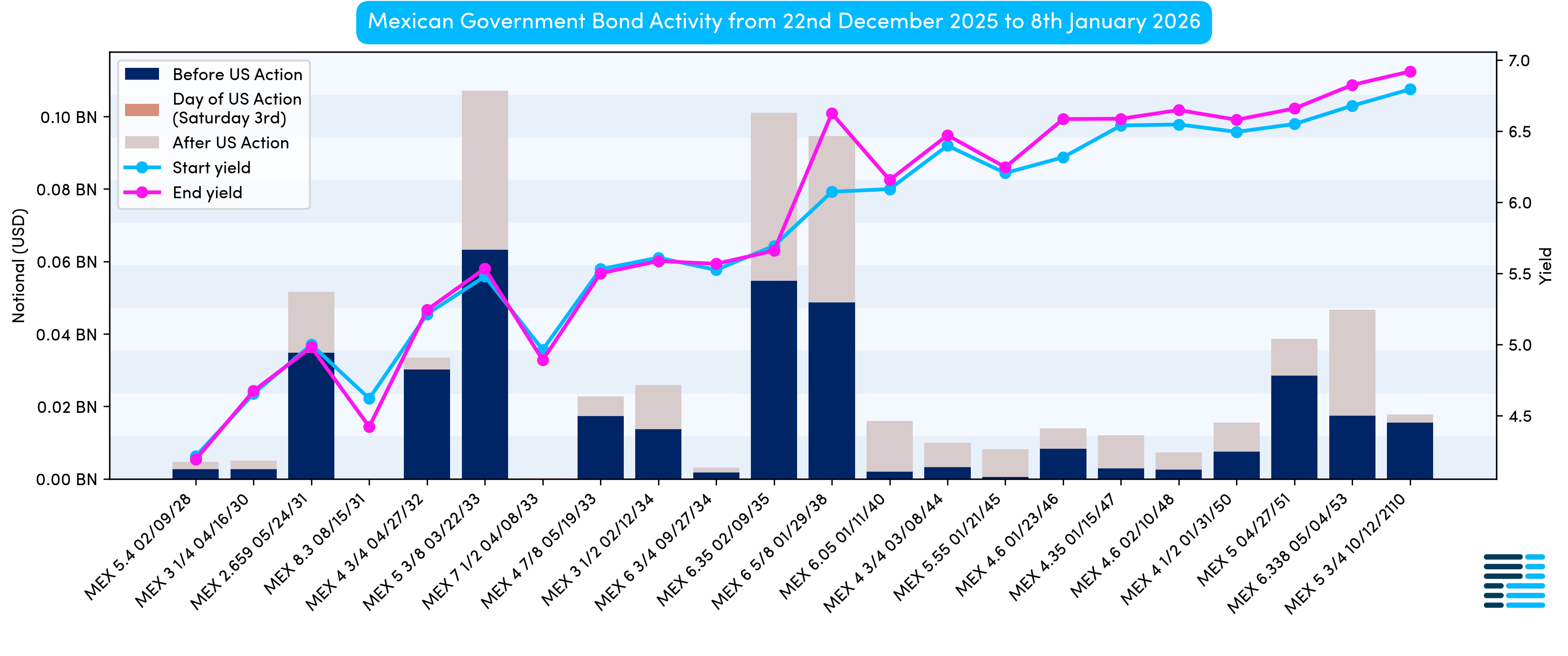

America’s southern neighbour was also mentioned in Trump’s speech3; hence, it is interesting to look at the bond market activity before and after.

It is important to mention that Mexico is a more frequent issuer than both Venezuela and Colombia (again focusing solely on USD-denominated bonds for now). Therefore, there are more data points available and, unsurprisingly, higher volumes reported, as illustrated in Chart 3.

Similar to Colombia, Mexico has a more traditional steep curve (i.e. the yield rises as the time to maturity increases). There has been some widening at various points; however, this is not universal, with yields at some tenors actually lower than before the announcement. Overall, it would appear that Mexican USD-yields have not moved significantly.

Volume tells a similar story in the sense that there was more flow across the curve at the end of December, than in the early part of January (again acknowledging that some aggregated data may still need to be considered in due course).

In summary, it would appear that (unsurprisingly) the largest movement has occurred on Venezuelan government bonds, with some impact on Colombia and little to nothing on Mexico. No data reported under MiFID are available for either Cuba or Greenland, so we cannot draw any conclusions on those markets. However, given we are only in the second week of 2026, it looks likely that having accurate and timely post trade data could be more important than ever before.

1https://www.reuters.com/world/americas/world-reacts-us-strikes-venezuela-2026-01-03/

2https://www.csis.org/events/what-just-happened-venezuela-and-what-comes-next

4https://thehill.com/homenews/administration/5672700-trump-venezuela-cuba-mexico-threats/

6https://www.bbc.co.uk/news/articles/c4g0zg974v1o

%20(5).png)

%20(4).png)