In recent times it has often felt as though there was a major election just around the corner, and whilst this can be captivating to some, plenty of people may feel a bit of election fatigue. When it comes to the bond markets however, elections always pique the interest of analysts and investors alike.

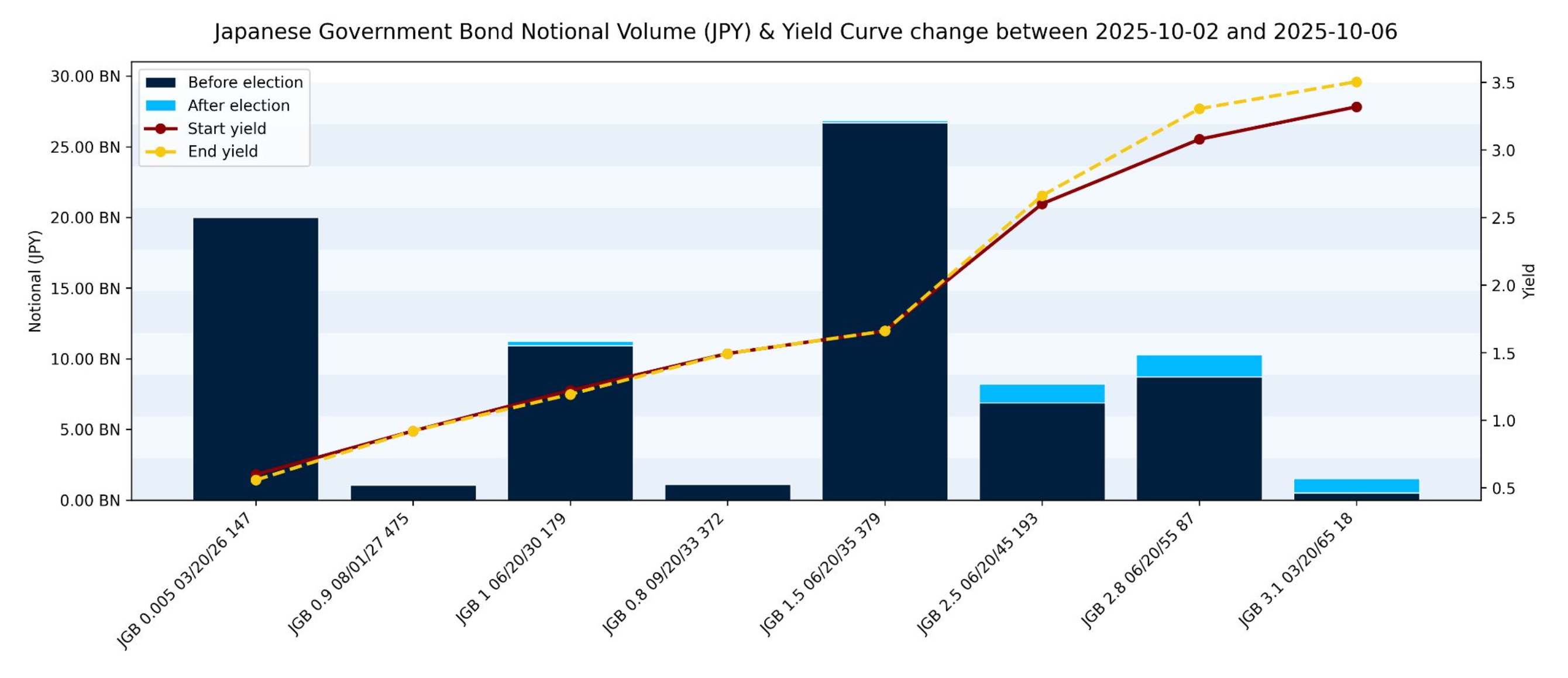

Over the weekend we saw Sanae Takaichi elected as the new Japanese prime minister1 and very quickly that got me thinking about the likely market reaction. By looking at a (working) day either side of the election, although there is an observable widening in long-end yields, very little volume was reported under MiFID in real-time.

Those familiar with the current MiFID reporting may well be aware that larger trades can sometimes be deferred and aggregated. This means the individual transactions are not made public to market participants, instead (when certain criteria are met) trades are grouped together, a VWAP price calculated and then the information is shown as a single block.

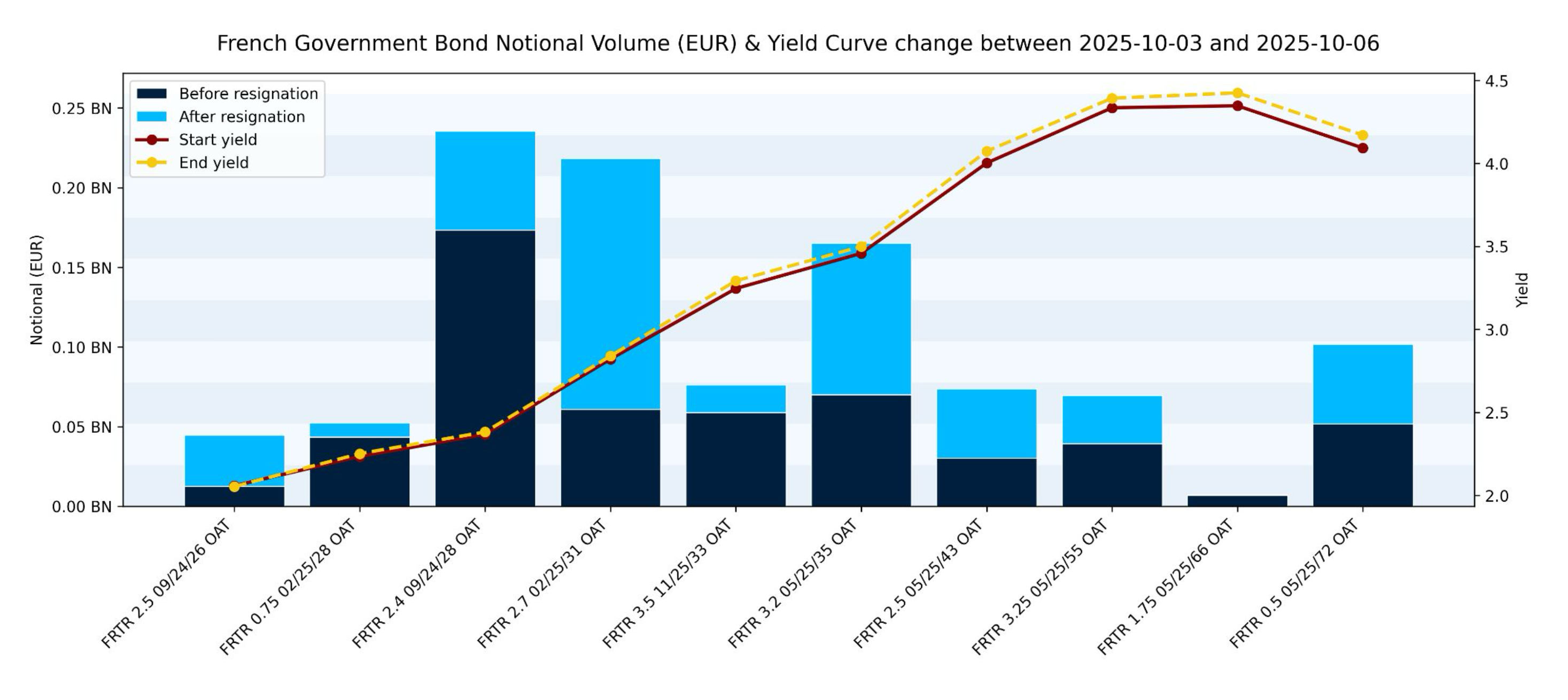

If we next turn our attention to France, where Prime Minister Sébastien Lecornu announced his resignation on Monday2, we can see a similar pattern, with long-end yields widening, but interestingly far more volume reported in real-time, after the news was widely known.

Again, it is likely there was still a significant amount of volume that did not show in real-time, due to the current dissemination rules, however this is changing! From December 1st, the new FCA transparency rules come into force, with one key aspect being the removal of ‘indefinite deferrals’ and aggregation3. Some sources are also predicting over 95% of trades will be disseminated to the public in near real-time4.

1https://www.bbc.co.uk/news/articles/cx2pmy7m72lo

2https://www.bbc.co.uk/news/articles/c749k11vnzgo

3https://www.fca.org.uk/publication/policy/ps24-14.pdf

4https://www.ft.com/content/2a43670c-967d-44be-80cc-6671b0c90c00?shareType=nongift

%20(5).png)

%20(4).png)