%20(2).png)

After more than a month, only two countries remain and whilst we need to wait until Sunday night to see who triumphs on the pitch, we can at least see who comes out on top in the debt markets with our World Cup Final Edition of Propellant Insights.

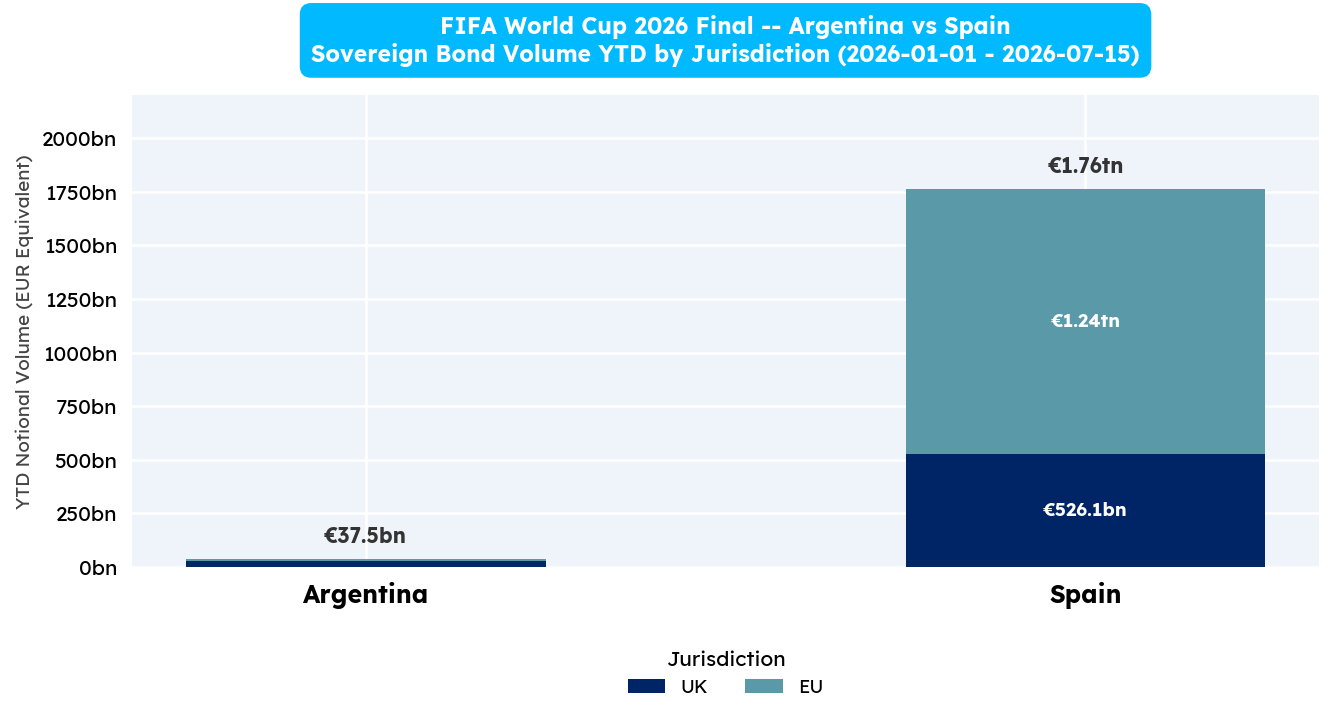

We kick off (pun very much intended) with year to date volumes between the two finalists and to use another sporting metaphor there is clearly a front runner.

Whether this translates to an on-the-pitch victory remains to be seen, but when it comes to absolute volumes reported under MiFID there is only one winner.

The clear disparity seen in chart 1 is unlikely to be a shock because the majority of Argentinian volume is likely to be traded in the Americas (with a reasonable amount in the US).

FINRA do not publicly disseminate (non-US) sovereign debt volumes, so we can not see USD Argentinian debt (traded in the US) via TRACE. However, even if we could, given the reliability of Spanish government debt, and Argentina’s history of default (see Insights Issue #2), it stands to reason that Spanish volumes would significantly outperform here.

It seems clear that Spain are ahead at the end of the first half, with a stunning outperformance in absolute volumes.

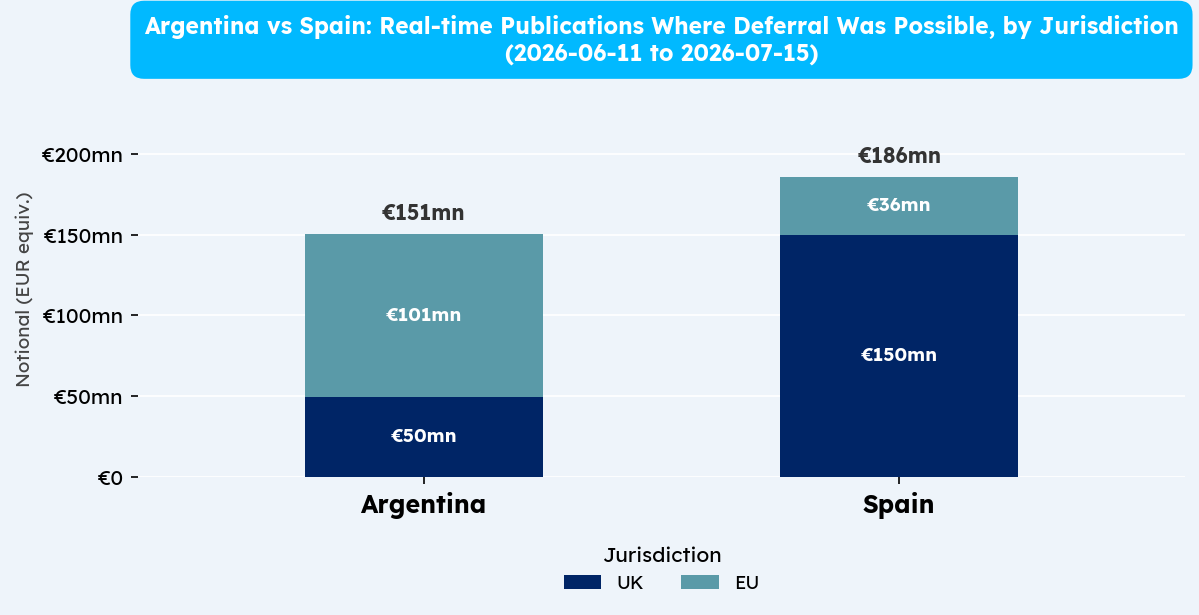

When it comes down to real-time publications it is perhaps much closer than expected.

Spain falls into the top tier for both the FCA and ESMA, meaning their debt is (generally) subject to shorter deferrals than other issuers.

What is surprising however, is that proportionally, the volume reported in real-time (where a deferral was possible) is not materially different between the two nations (around EUR 35 million equivalent).

Perhaps more interesting is that the Spanish flow reported earlier than expected is typically out of the UK, whereas for Argentinian debt it is out of Europe (this is most likely due to the differing reporting rules and deferral timelines).

This may come down to Value at Risk (the less controversial VAR) and in a shocking twist Argentina takes the second half by the thinnest of margins, with a smaller amount of activity reported ahead of expectations, so extra time here we come...

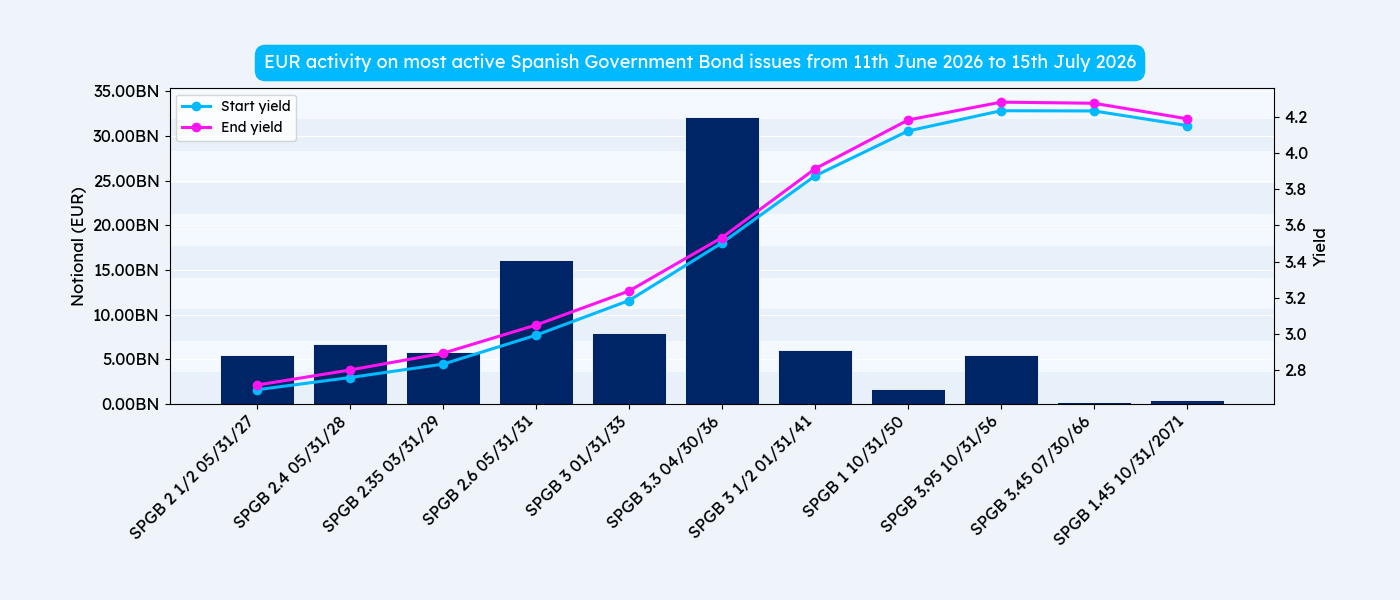

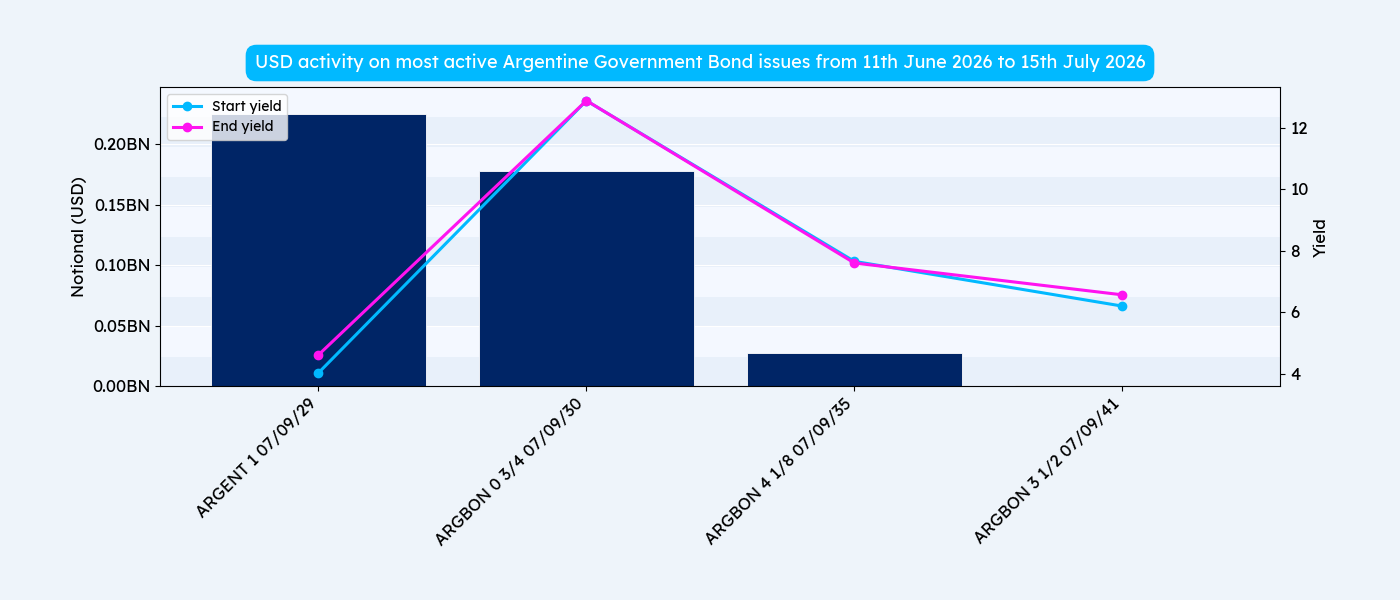

As the nerves begin to tingle, the liquid issues step up to cement their place in history...

An exceptionally smooth yield curve (with no stuttering run up) and only a very gentle widening over the tournament, it could be all over... Argentina responds with another gentle widening, but the absolute yield and lower volumes swing it in Spain’s favour!”

Original photograph taken by Richard Hadley

Dan Barnes - Dan is a highly experienced market commentator and founder of multiple media ventures including Trader TV and The Desk.

He is contributing as a guest editor for Propellant Insights ahead of starting a new venture in Q4 this year.

Vidal Mehra - Vidal is Chief Product Officer for Propellant Digital and the lead author for Propellant Insights.

He has been working with financial institutions for over 20 years across multiple disciplines including front office and consulting roles.

Helena Roughton - Helena recently joined the team as a Product Manager, bringing extensive MiFID policy experience having previously worked at AFME.

She also brings product remediation and data analysis experience from the Bank of New Zealand.

%20(5).png)

%20(4).png)