Whilst there has been plenty of excitement surrounding the upcoming transparency changes, soon to be implemented by the FCA1 and ESMA2, the main focus has been on bond transparency.

Real-time reporting for corporate and sovereign bond transactions is forecast to be as high as 85% and 96% respectively3. However, to date far less focus has been on the changes to Interest Rate Swap (IRS) transparency (which follow the same timeline).

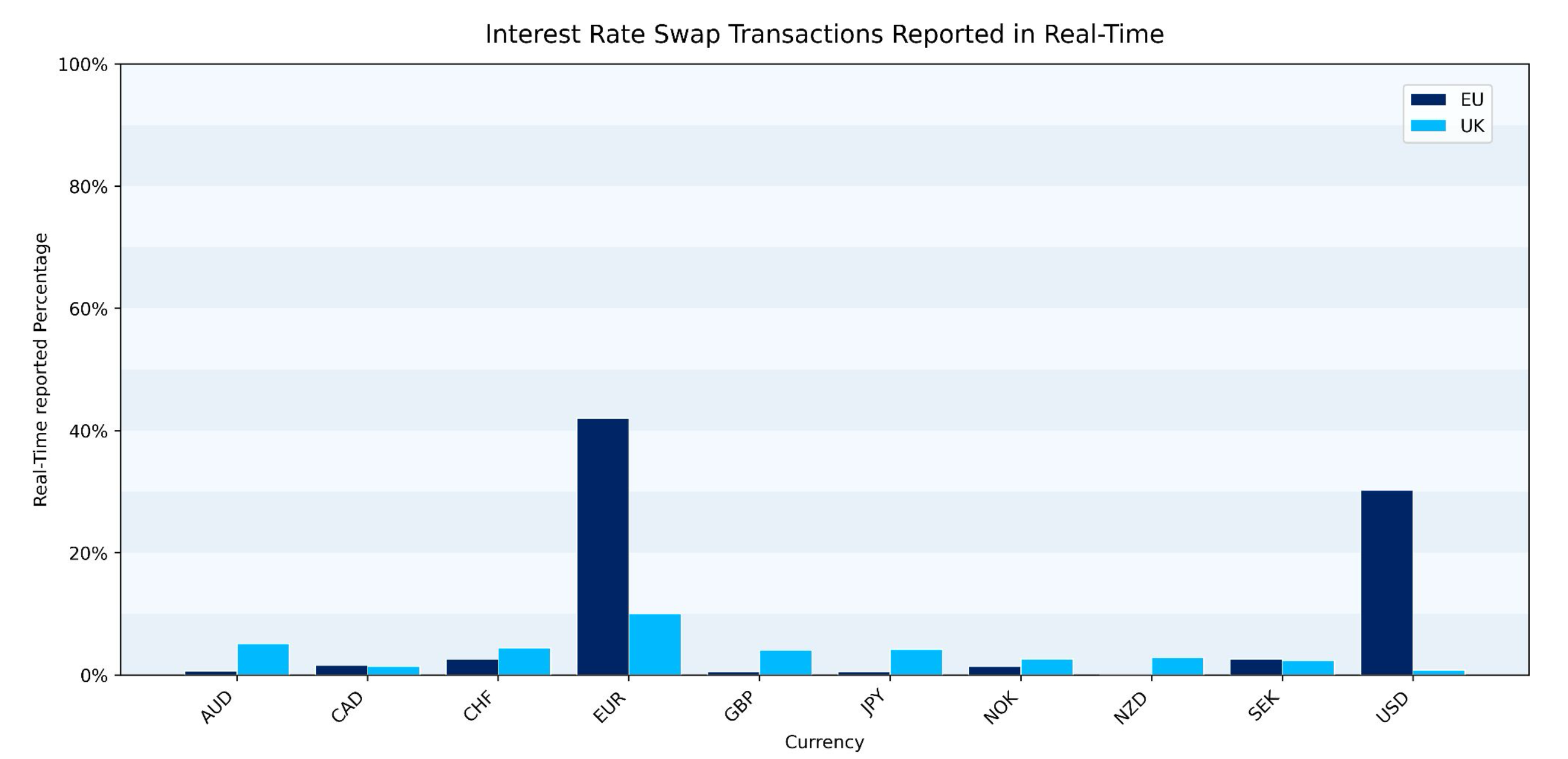

When comparing G10 currencies, it is clear that EUR- and USD-denominated swaps have a far higher percentage of average (mean) transactions reported in (near) real-time than all others, which is hardly surprising. However, when we switch focus to notional volumes, it becomes interesting.

Currently, as with bonds, the majority of IRS transactions are reported with a delay (up to 89% of EUR IRS notional volume is reported with a four-week deferral4).

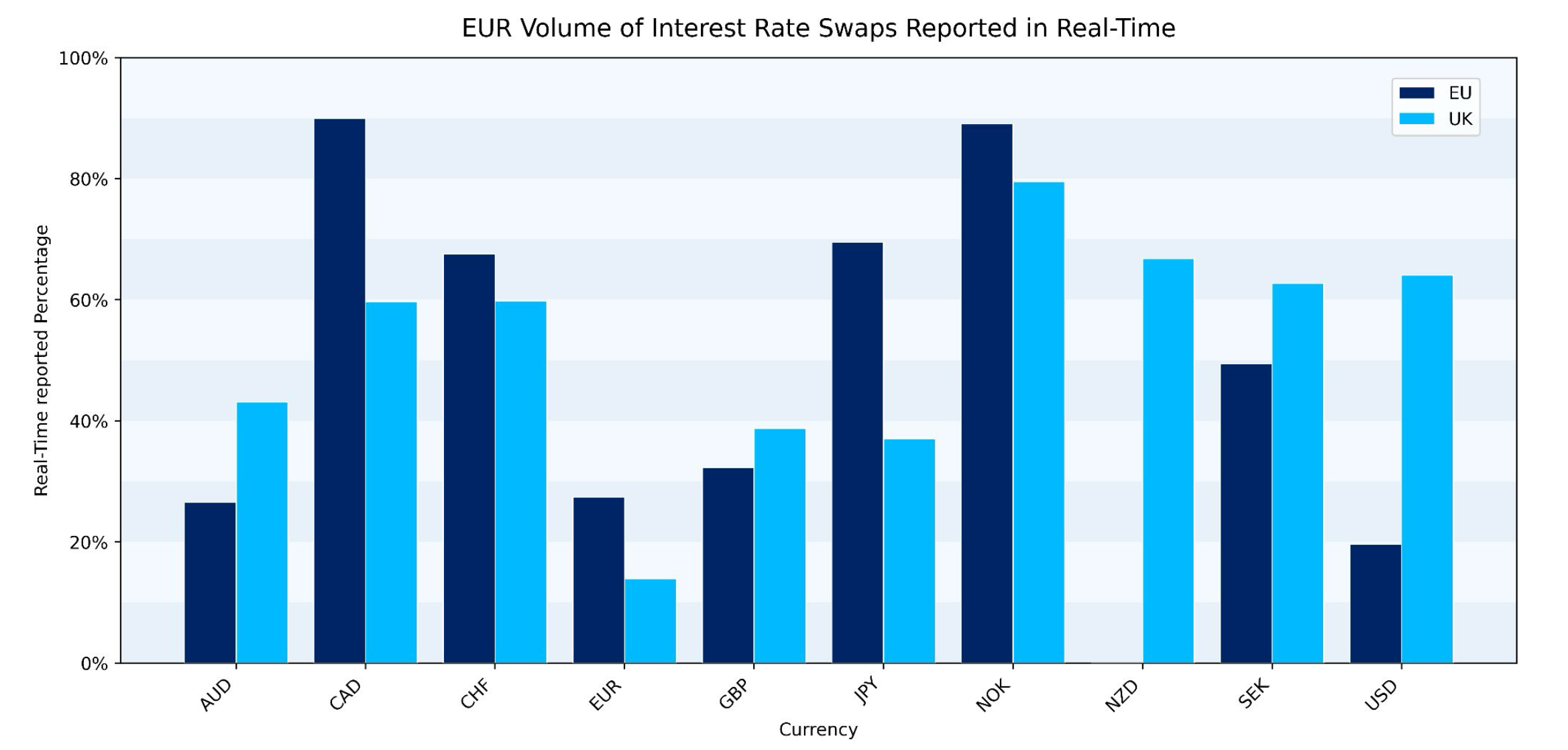

From Chart 2, it is evident that both EUR and USD real-time reported volumes on ESMA venues are lower than the percentages of respective transactions. This is likely because most larger EUR- and USD-denominated transactions may be executed via US Swap Execution Facilities and reported via a Swap Data Repository.

Across the other G10 currencies, only a small percentage of trades are reported in real-time, whilst the real-time percentage of notional volumes is much higher. This is likely due to a smaller transaction count, meaning a number of large tickets can significantly skew the result. Additionally, it is important to note that a large portion of notional volume may be executed on non-MiFID venues and therefore the data may not appear here.

In order to capture a more complete view of the market, it is necessary to include data from US Swap Data Repositories such as DTCC, which is something that can be enabled for Propellant Digital clients, so please get in touch to find out more.

1https://www.fca.org.uk/publication/policy/ps24-14.pdf

3https://www.ft.com/content/2a43670c-967d-44be-80cc-6671b0c90c00?shareType=nongift

4https://www.clarusft.com/what-we-need-to-do-to-fix-mifid-ii-data/

%20(5).png)

%20(4).png)