.png)

ESMA’s new bond transparency regime has been in effect for over one month, meaning that the larger trades (deferred for 4 weeks) are now starting to show in the data.

We can also begin to build a picture of whether the expected deferral time matches the actual deferral time.

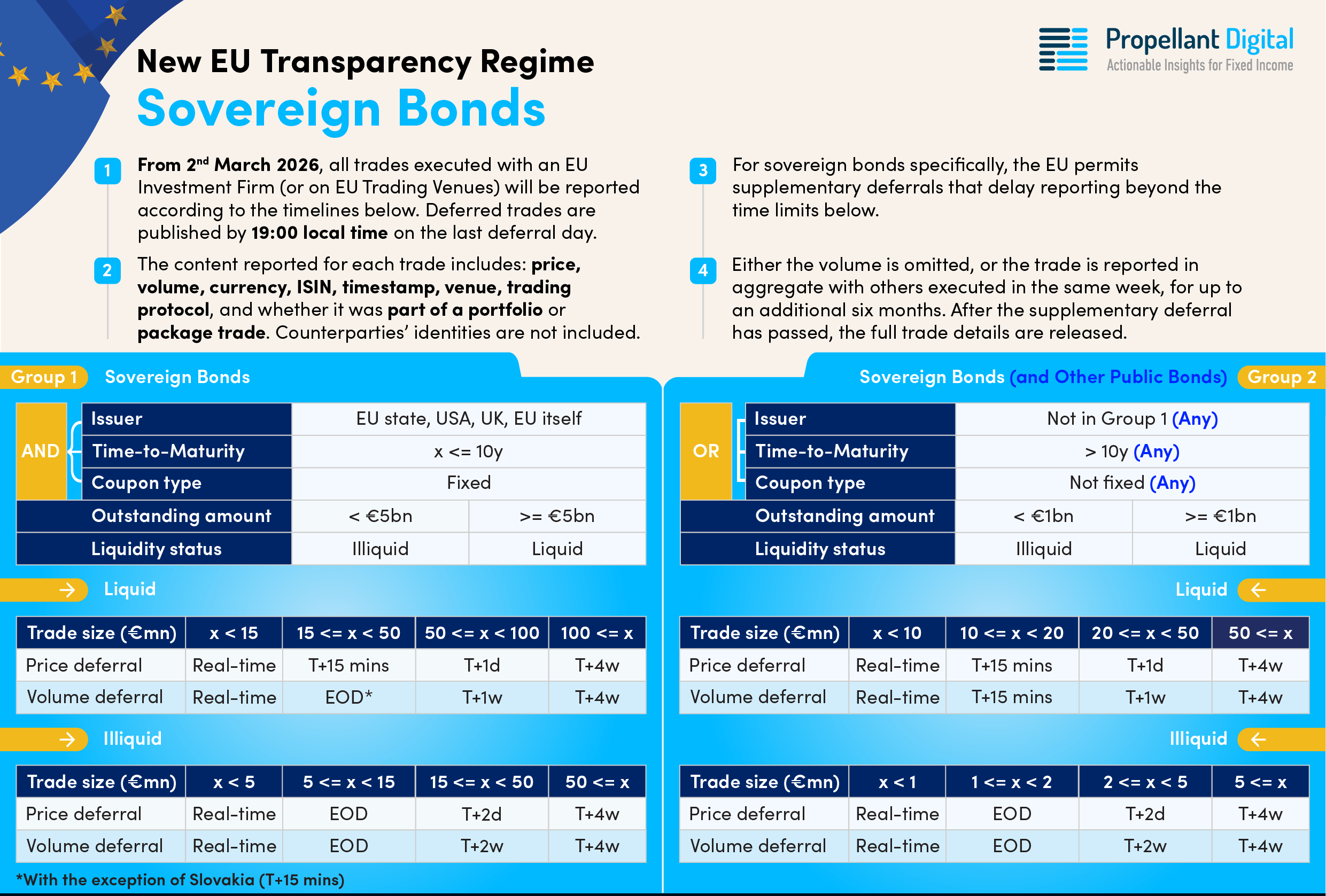

This week, we focus on Sovereign Bonds reported under ESMA’s new transparency regime (which went live on 2 March 2026). To recap, the new regime changed the deferral approach by removing the notion of indefinite aggregation, ensuring that market participants will now always see a transaction-level report for every trade.

A quick summary of the new deferral rules for Sovereign Bonds is shown in Figure 1:

Following a review of the sovereign deferral rules, the focus now turns to the data, which shows how the percentage of transactions reported in real-time differs across the various categories (see Chart 1).

.png)

EGB near-time reporting (defined here as 15 minutes or less) has increased to around 90% of all transactions (up from approximately 65% in March/April last year). For European Union-issued bonds, the movement has been even more pronounced, doubling to approximately 70%. UK Gilts surprisingly show the largest percentage increase, from circa 20% to around 95% now reported in under 15 minutes. US Treasuries follow a similar pattern to EU bonds, whilst the remainder (limited here to EUR-, GBP- and USD-denominated bonds) have more than quadrupled, from around 15% to approximately 65%.

It is interesting to note that some predictions forecast a real-time in excess of 90%1, post the introduction of the consolidated tape(s). Whilst there is still some time before the UK and EU tapes are launched, we can see that transparency has already vastly increased under the new (ESMA) regime. Whilst the increase in near-time reporting is notable, it is important to consider if trades are being reported in the intended fashion.

Chart 2 below contains data only for ESMA trades reported with no deferral flag; this means they should be disseminated in real-time.

.png)

The green and blue sections make up the vast majority of activity (as expected), showing that whilst most trades are reported in under 1 minute, some still take up to 15 minutes before being shown to the wider market. This is most likely caused by slower-than-expected booking procedures.

What is perhaps more interesting, is the small (although in excess of 15% in some categories) percentage of trades reported at the end of the day (or even later) without a deferral flag. This could be due to multiple factors and cannot be determined with certainty; however, the most plausible explanations are:

Having considered trades with no deferral flag, we will next examine trades with the appropriate flag to suggest they were intended to be deferred by 15 minutes.

Chart 3 below contains data only for ESMA trades reported with the Medium Liquid or Medium Illiquid deferral flags, this means they should be disseminated to the market after 15 minutes.

.png)

Whilst a small portion of these trades actually get reported in real-time (despite having the appropriate deferral flag), the majority do receive the expected 15-minute deferral.

Of greater interest is the proportion of trades that are booked later. These are typically still booked on the same day, before 17:00 UTC, but not always. As shown, all categories (particularly 'Other Sovs') have a noticeable amount of tickets booked after 17:00 on the trade date. There are likely to be perfectly logical explanations for this, with the reasons being similar (if not identical) to those shown on the previous page, for real-time trades being unintentionally delayed.

It should also be noted that, whilst every effort has been made to remove cancel/amends (so as not to skew the timescales), it remains possible that some trades could fall into that category, slightly over estimating the percentage of trades booked late.

This will continue to be monitored and we will produce further insights into both the ESMA and FCA transparency regimes in a few weeks once more data becomes available.

%20(5).png)

%20(4).png)