A bond trade report, which could be deferred for three months, is actually being reported in near real time, due to inconsistency in the way venues and their APAs report trades. This could unexpectedly result in information leakage. The new FCA and ESMA transparency frameworks are now fully embedded, and so these discrepancies are occurring despite clearly defined deferral rules.

The FCA launched its new transparency regime in December 2025, with ESMA following in March 2026. The former focused on both debt instruments and OTC derivatives, whereas the latter focused solely on debt instruments (ESMA have outlined some changes for OTC derivative reporting which are expected to come into play in early 2027).

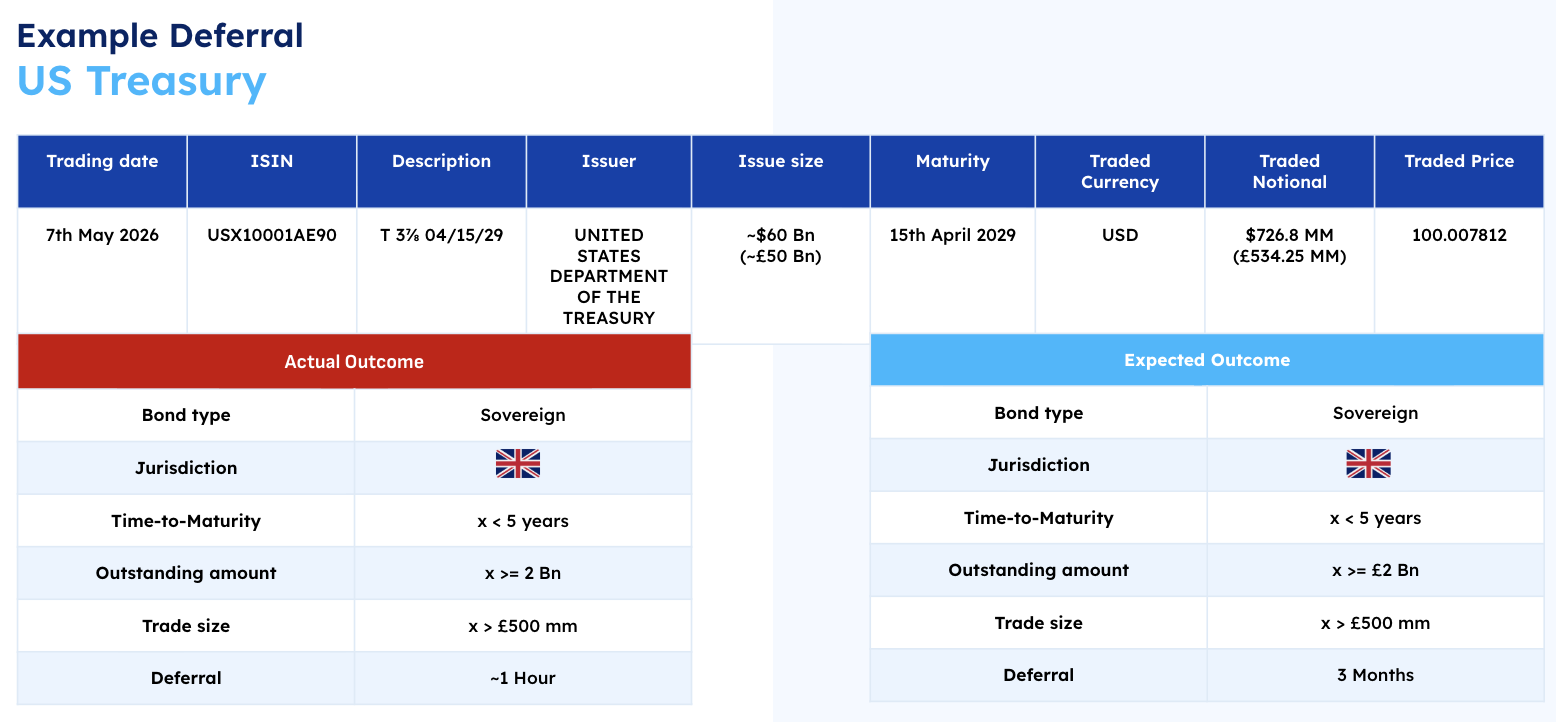

When a trade is reported, market participants expect all venues to follow the same rules (and presumably they do), however the outcome is not always the same. If a trade report is expected to be deferred for several months, and is in fact disclosed in real time, dealers may widen their bid ask spreads to reduce the risk associated with taking on large positions that are instantly made public. Below we highlight an example of the same bond being treated differently by two venues.

The above example shows a trade that was reported in near real-time (within the hour), yet it would appear to have been eligible for a deferral of 3 months (the longest permitted under the new FCA transparency framework).

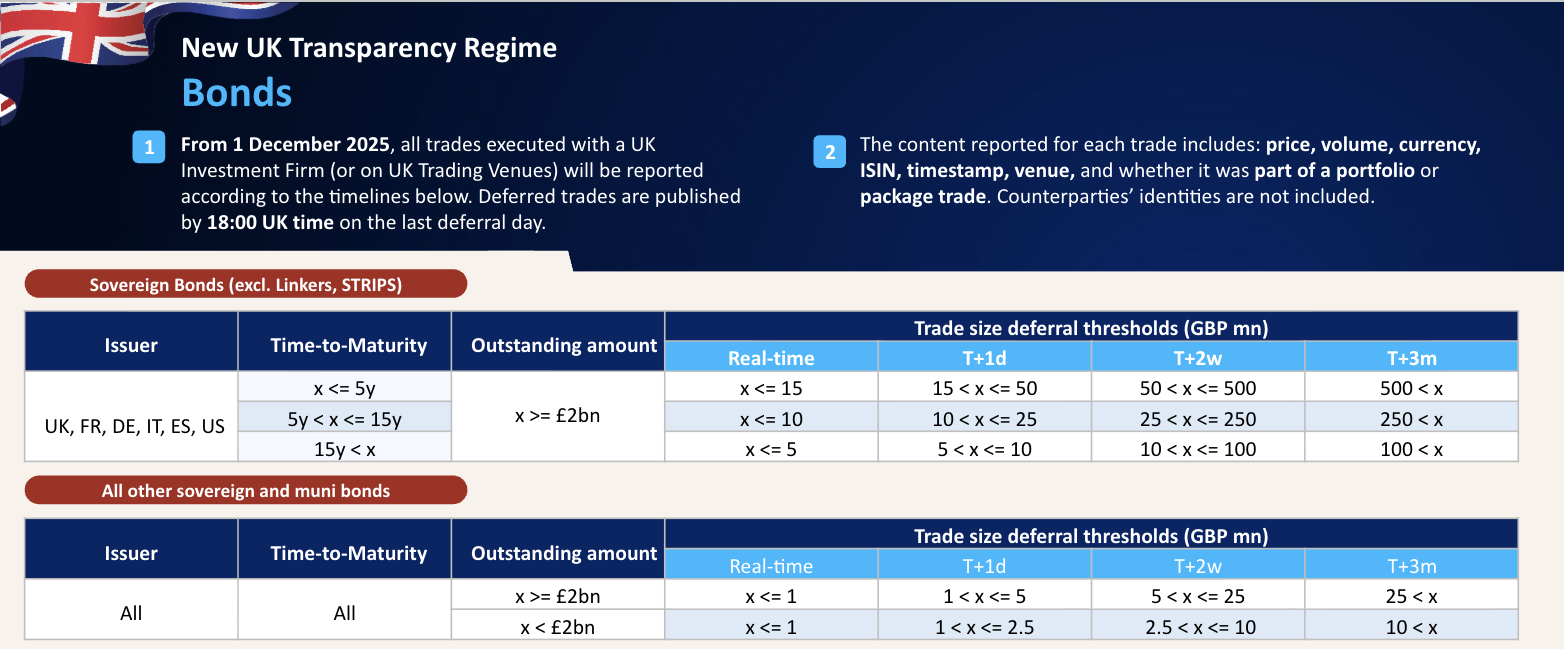

Before diving into the data we like to provide a brief summary of the transparency changes. Starting with the FCA, the new deferral rules for Sovereigns and Public Bonds are outlined in Table 1 below.

The FCA has 6 sovereign issuers in its top liquidity group:

In order to qualify for this top group a bond must be issued by one of the above, have a fixed rate coupon, an outstanding amount (at the time of trading) of GBP 2 billion equivalent or more and not be inflation linked or a strip.

The second group contains all other sovereign bonds, along with bonds issued by public sector issuers such as municipal bonds and SSA’s.

The deferral time for this second category is simply determined by the outstanding amount at the time of trading (i.e. less than GBP 2 billion equivalent or not).

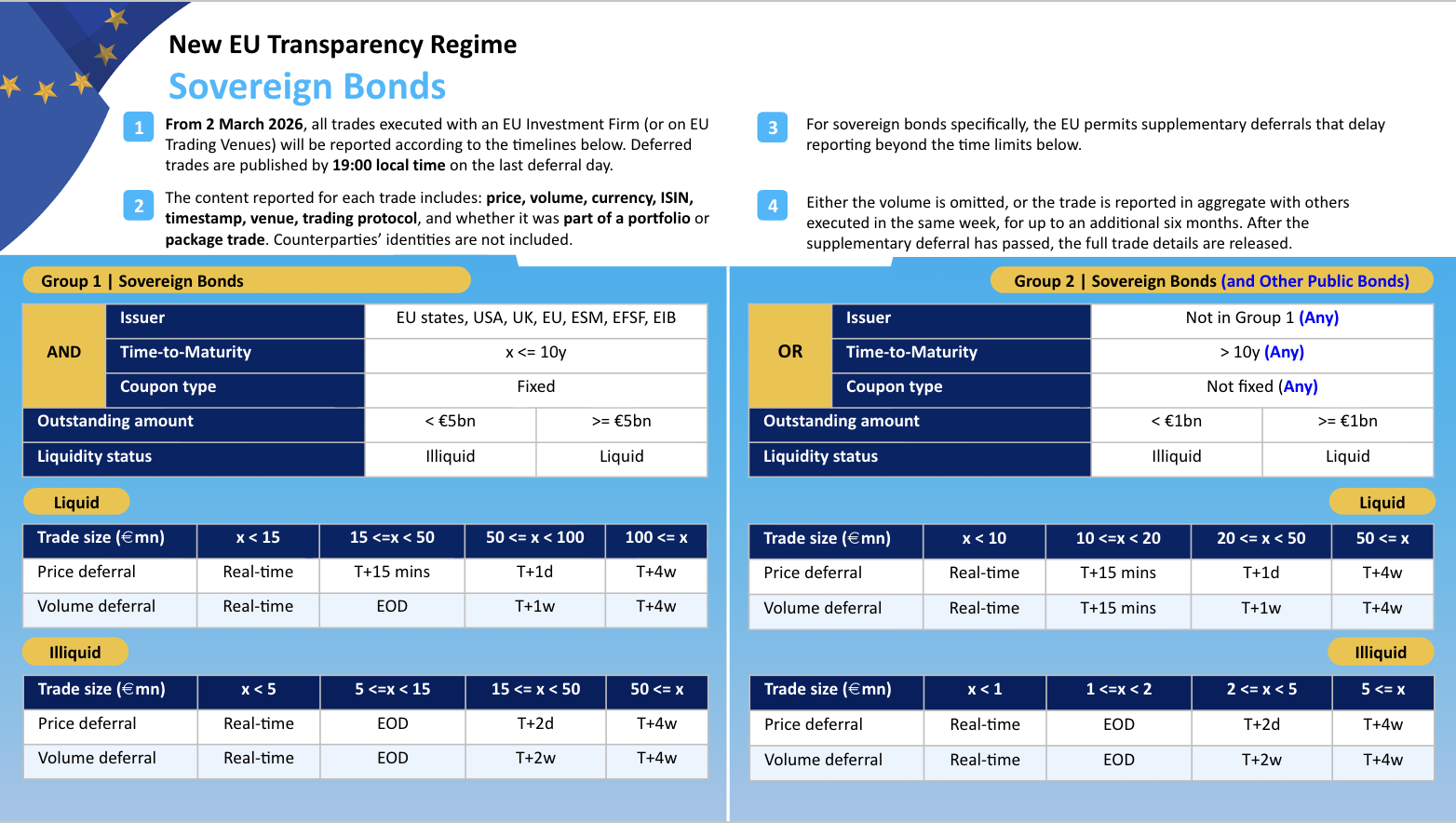

ESMA takes a not dissimilar approach, however the rules are not identical, as can be seen in Table 2 below.

ESMA of course has a far wider geographical remit to consider, so ESMA’s Group 1 includes the following issuers:

In order to qualify for Group 1, a bond has to be issued by one of the above, must have 10 years or less to maturity and must have a fixed rate coupon (this also excludes strips and linkers). Additionally ESMA has a liquidity assessment, purely based on the outstanding amount (at the time of trading), which splits bonds into liquid or illiquid (for Group 1 the split is EUR 5bn equivalent or over to be deemed liquid).

If the above conditions are not fully met, then a sovereign (or public) bond would fall into ESMA’s Group 2 (shown on the right hand side of Table 2 above).

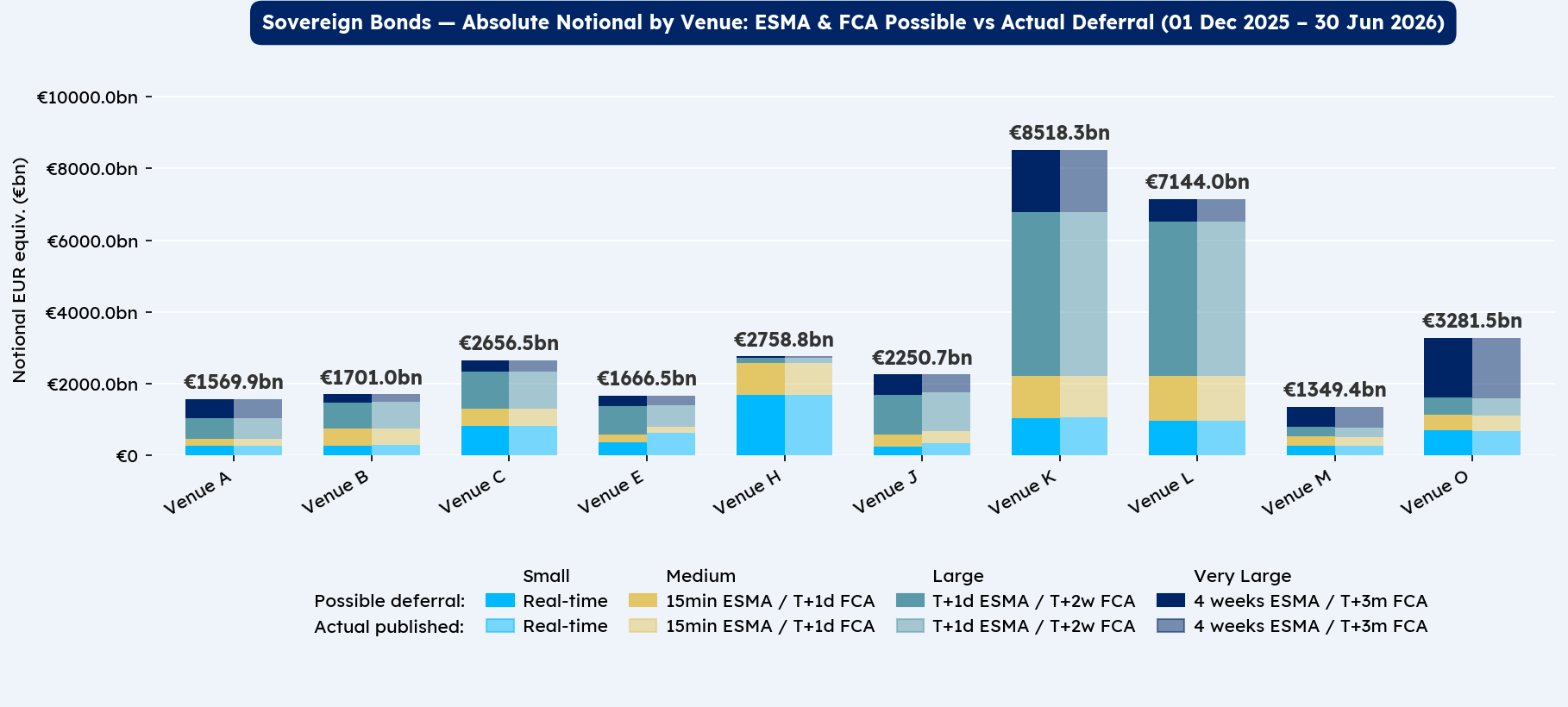

We now turn our attention to the data. Our aim here is to determine whether venues (and APAs) are reporting in-line with expectations.

At a glance we can see in Chart 1 that trading venues and APA’s do typically report in the timeframe we would expect.

Whilst we can see that in absolute notional terms most venues report in-line with expectations, we can see some slight discrepancies on venues E and J.

Over the page we will consider a normalised approach (looking at the percentage for each venue) and see if that highlights anything further.

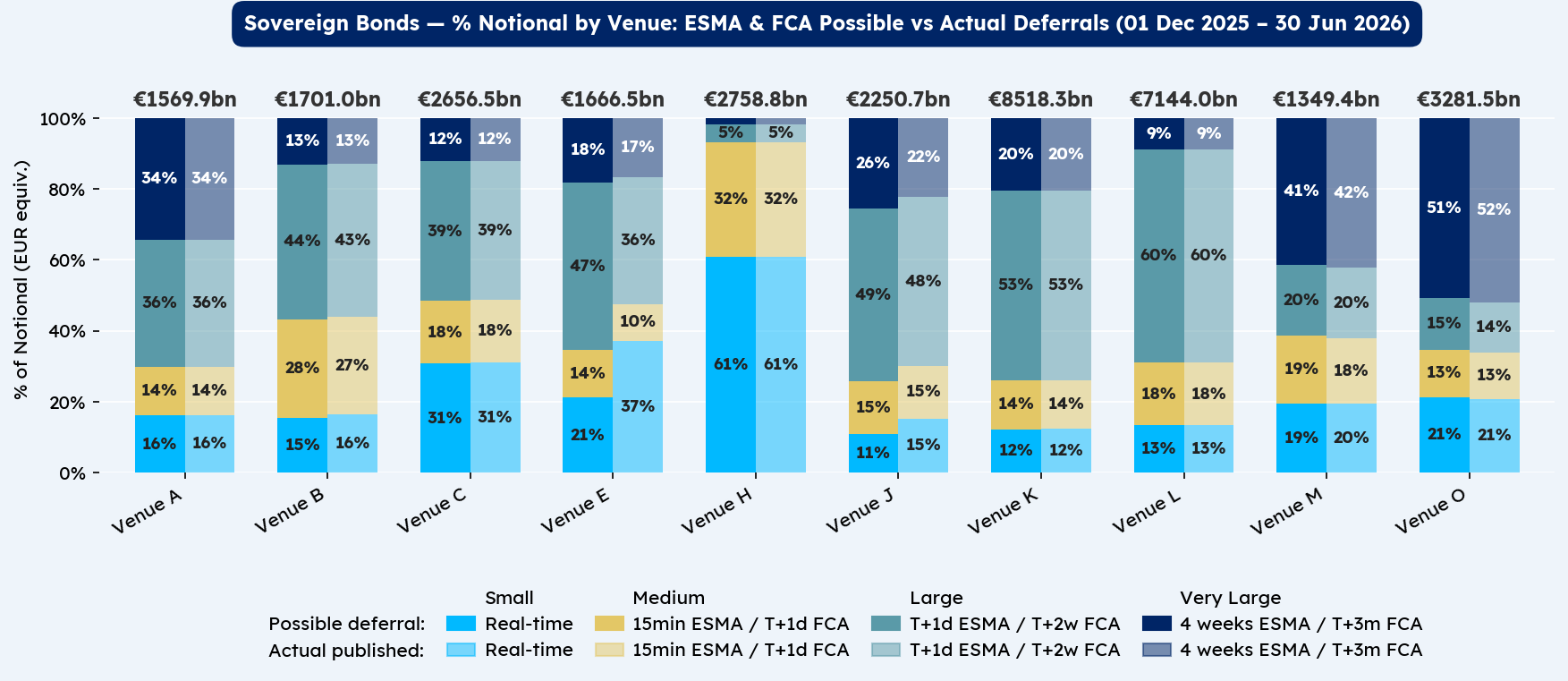

Below in Chart 2 we can see a normalised view, showing the percentage breakdown by deferral bucket.

Whilst most venues have some discrepancies between actual and expected reporting timelines, the only venues that have a material difference are E and J.

For most venues, the discrepancy is in the region of 1% (or lower), so we can see it is immaterial, however considering this normalised view shows us that two venues do have mismatches, particularly venue J.

Next we consider the scale of these mismatches and consider what could be the cause.

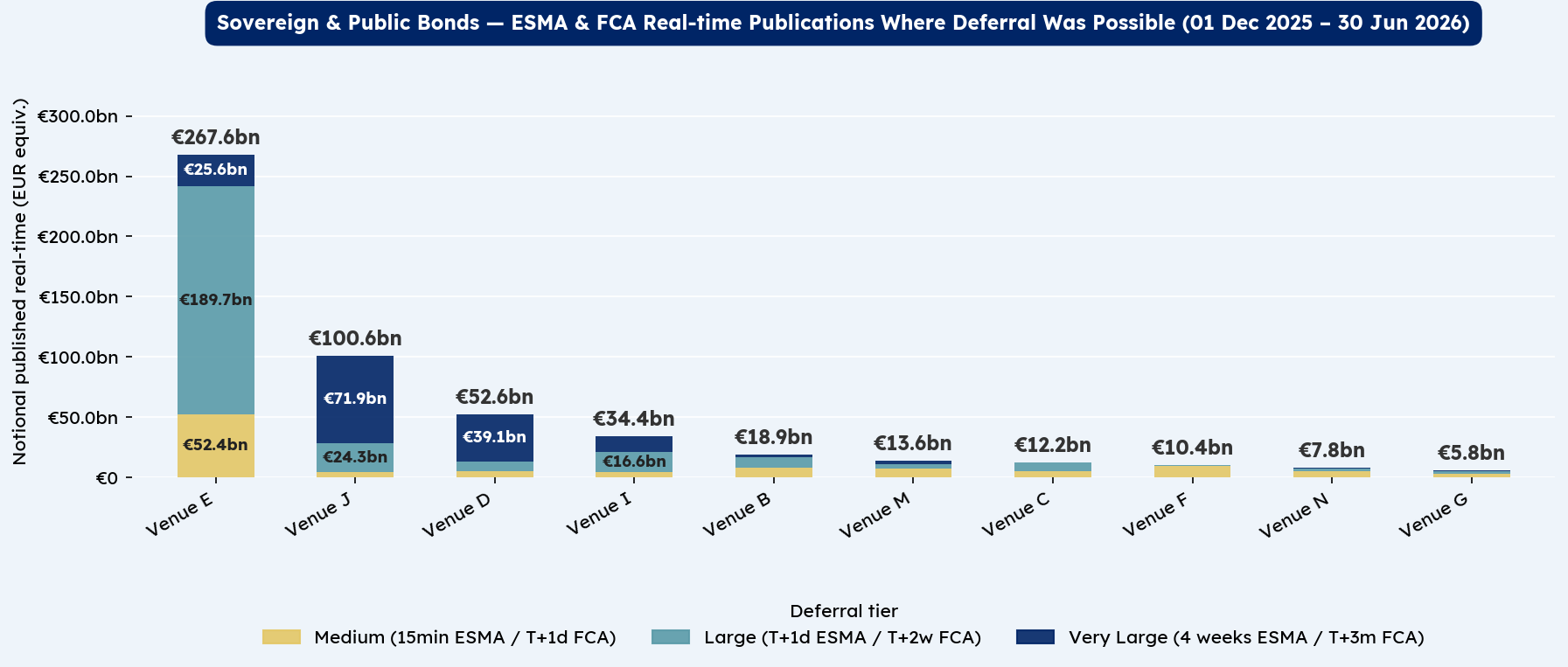

We finish up this week by looking at the venues based on the delta between the actual publication time and the expected.

Venue’s D, E & J stand out, with these reporting in real-time when a deferral could have been applied far more frequently than the others (Venue E in particular).

Now it should be stressed that within MiFID it is perfectly permissable to report quicker than expected (each deferral is the maximum time permitted before a report should be disseminated, not the minimum), however it is plausible market participants may not expect this behaviour.

“Venues are within their rights to publish trades in real-time if they wish, however the rationale behind this is still up for debate. It may be a conscious decision by some venues, aiming to increase real-time transparency, however anecdotal evidence suggests it is more likely that different venues use and interpret reference data in different ways, leading to unexpected outcomes in some situations.

Buy- and sell-side heads of desk would do well to understand how a venue or APA might choose to defer publication, rather than assuming maximum deferral will always be adhered to, as this could make a material difference to their trading costs.”

Original photograph taken by Richard Hadley

Dan Barnes - Dan is a highly experienced market commentator and founder of multiple media ventures including Trader TV and The Desk.

He is contributing as a guest editor for Propellant Insights ahead of starting a new venture in Q4 this year.

Vidal Mehra - Vidal is Chief Product Officer for Propellant Digital and the lead author for Propellant Insights.

He has been working with financial institutions for over 20 years across multiple disciplines including front office and consulting roles.

Helena Roughton - Helena recently joined the team as a Product Manager, bringing extensive MiFID policy experience having previously worked at AFME.

She also brings product remediation and data analysis experience from the Bank of New Zealand.

%20(2).png)