UK flicks the transparency switch: Real-time volumes surge on day 1

.png)

The new UK transparency regime for bond and derivatives markets comes into effect on 1 December 2025, marking a significant development in UK market structure. Average real-time transparency increased markedly, from 4% of volumes to around 26% when the new regime begins. This reflects not only a material step-change in how much volume is reported, but also a significant improvement in what is reported, with several additional data fields now available (see Table 1).

To understand how trading activity is shifting under the new regime, the Propellant team conducted intraday analysis across sovereign and non-sovereign debt, Interest Rate Swaps (IRS), and Credit Default Swaps (CDS). The analysis is carried out at multiple intervals during the trading day (12:00, 14:00, and 17:00) to capture the evolving patterns.

If your organisation is looking to analyse these data and assess how the new transparency regime may affect trading strategies, please complete the form and submit your enquiry. Propellant will be pleased to support your analysis.

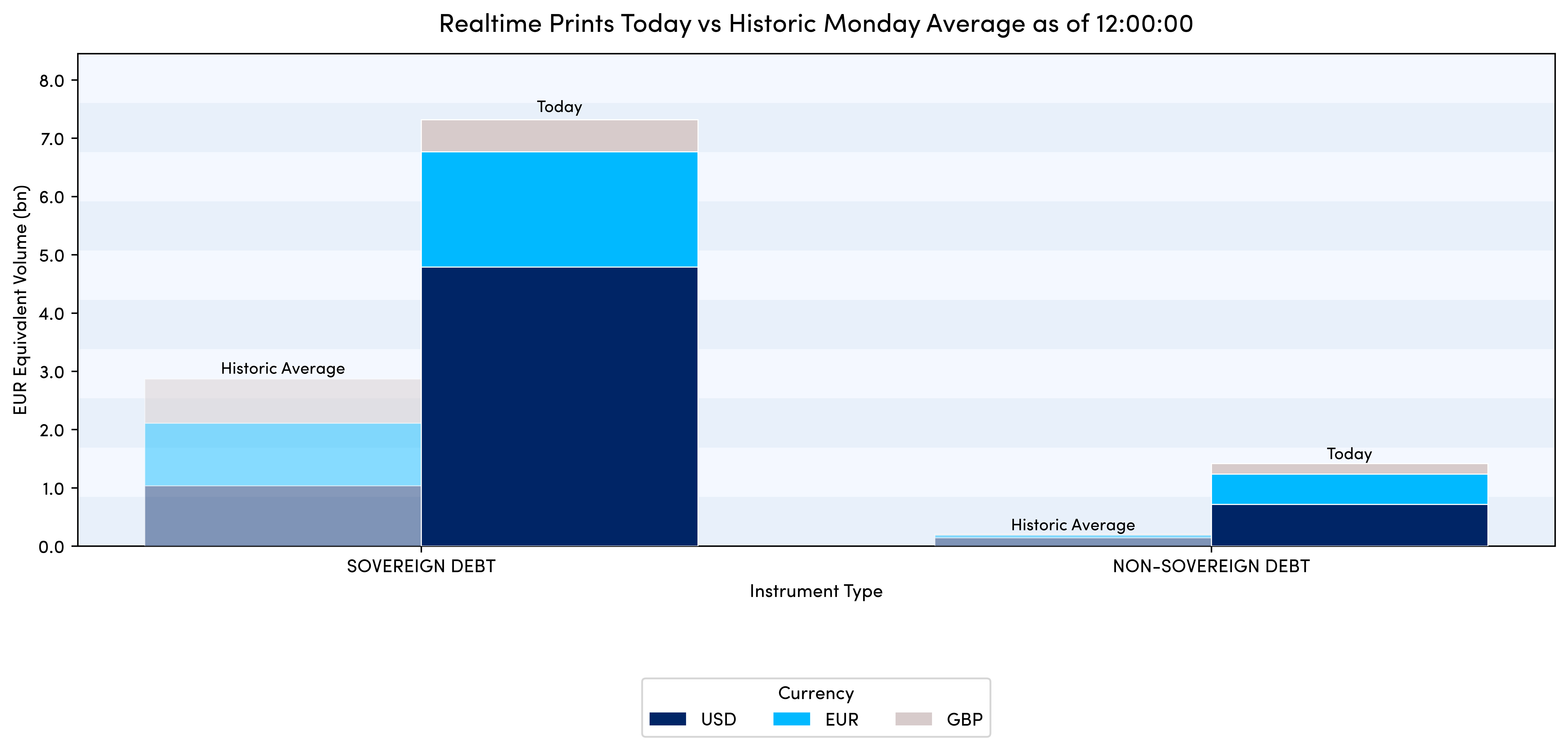

1. Sovereign debt and Non-Sovereign debt activity at midday

As shown in Chart 1, the impact on debt markets is already pronounced

- Sovereign debt volumes are approximately 50% higher than a typical Monday, based on average volumes by 12:00 PM across all Mondays in 2025.

- Non-sovereign debt volumes are almost 4x higher than is typical by this time of day.

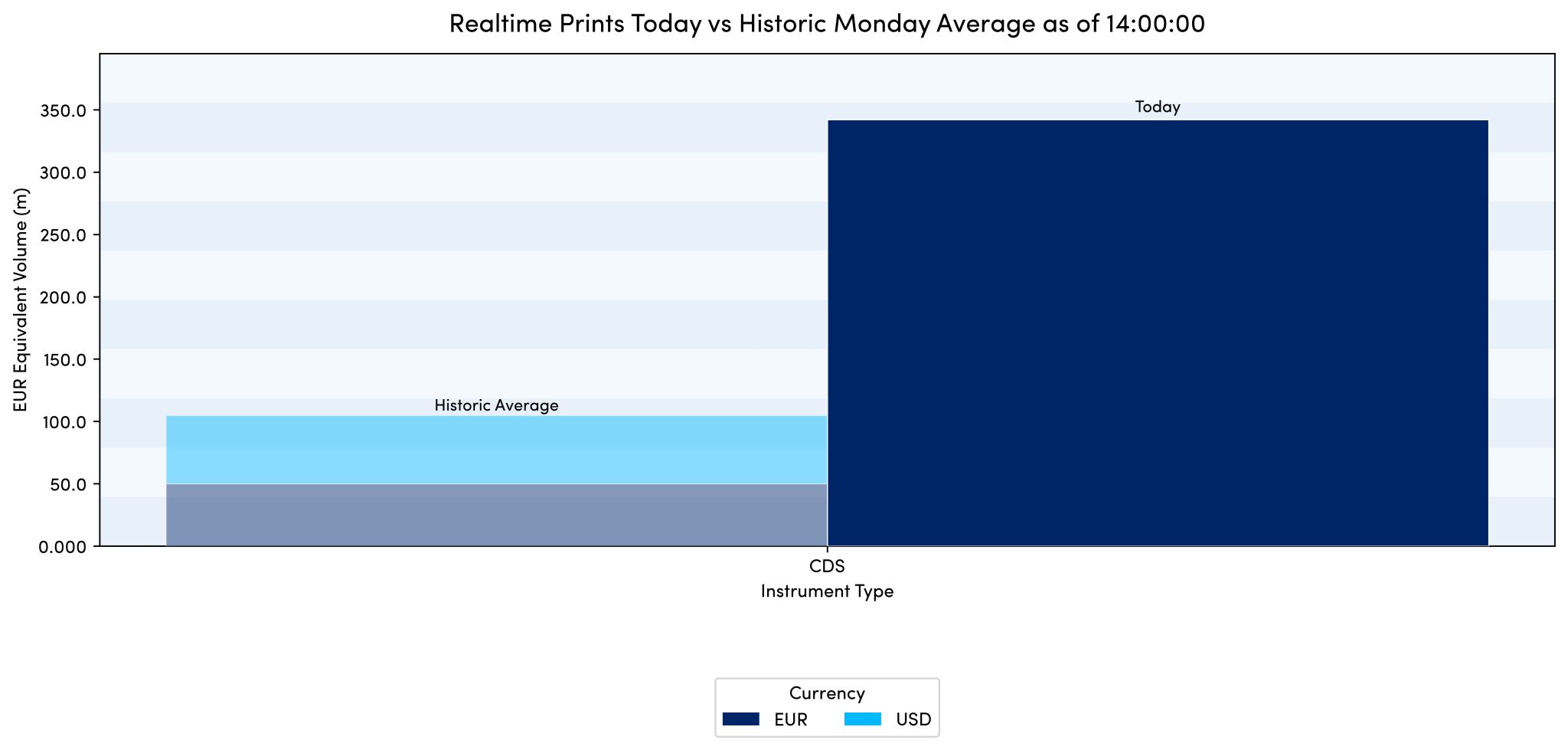

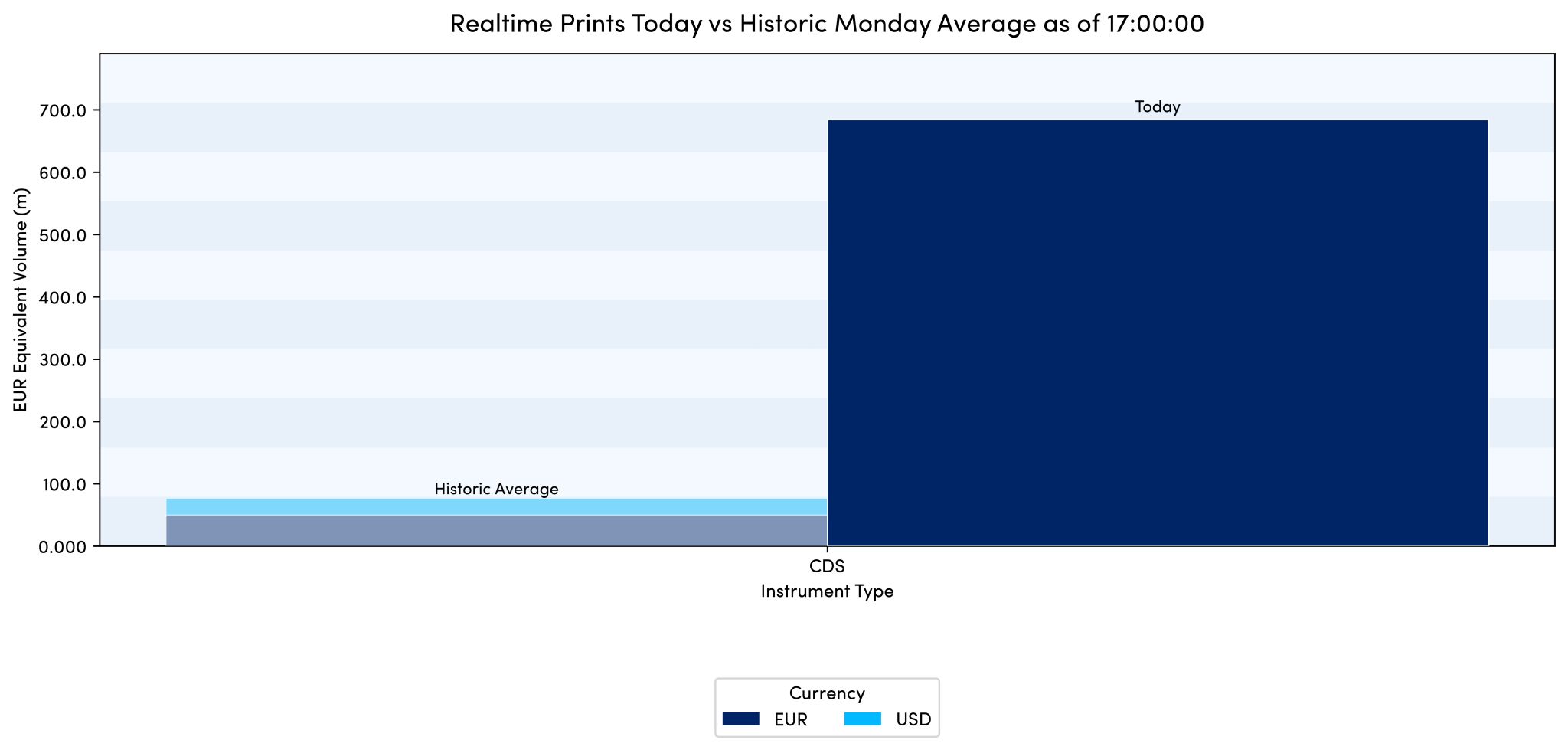

2. IRS and CDS activity at 14:00

Even though fewer contract types are in-scope, the greater requirement to report in real-time means the volumes are nearly 10 times higher than a typical Monday at this point in the trading day (see Chart 2). When it comes to Credit Default Swaps (CDS), only Index CDS are now mandatory reportable. Thus, not only are overall volumes three times higher (see Chart 3), but the composition of contracts is different, with volumes now almost exclusively concentrated on the EUR-denominated iTraxx indices (whereas historically, there is a lower volume per contract reported in real-time across a wider range of contracts).

Additionally, the availability of new fields, specifically the effective date and maturity date make it far easier to identify and group trade volumes for 10Y SOFR swaps, 5Y EURIBOR swaps, and other reference rates.

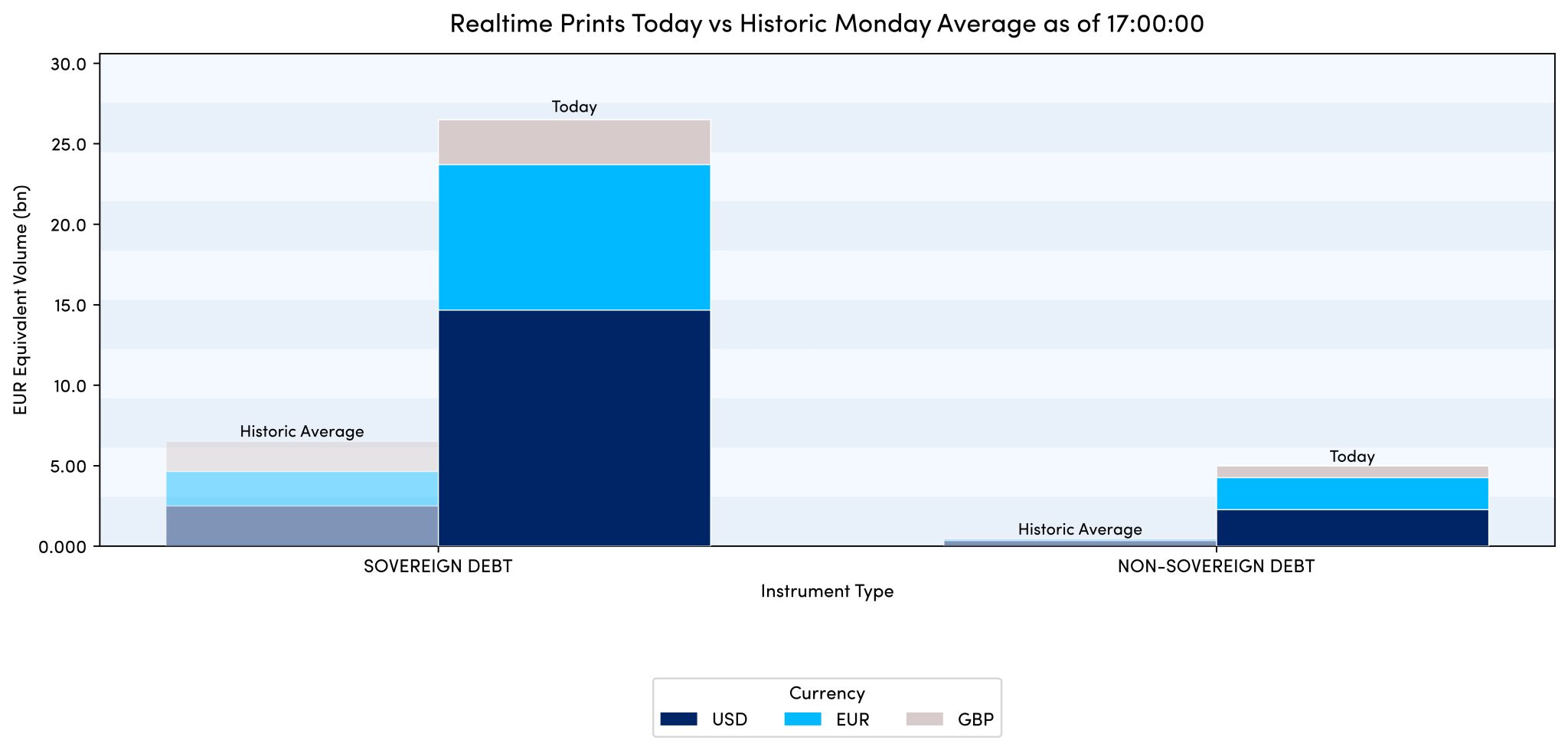

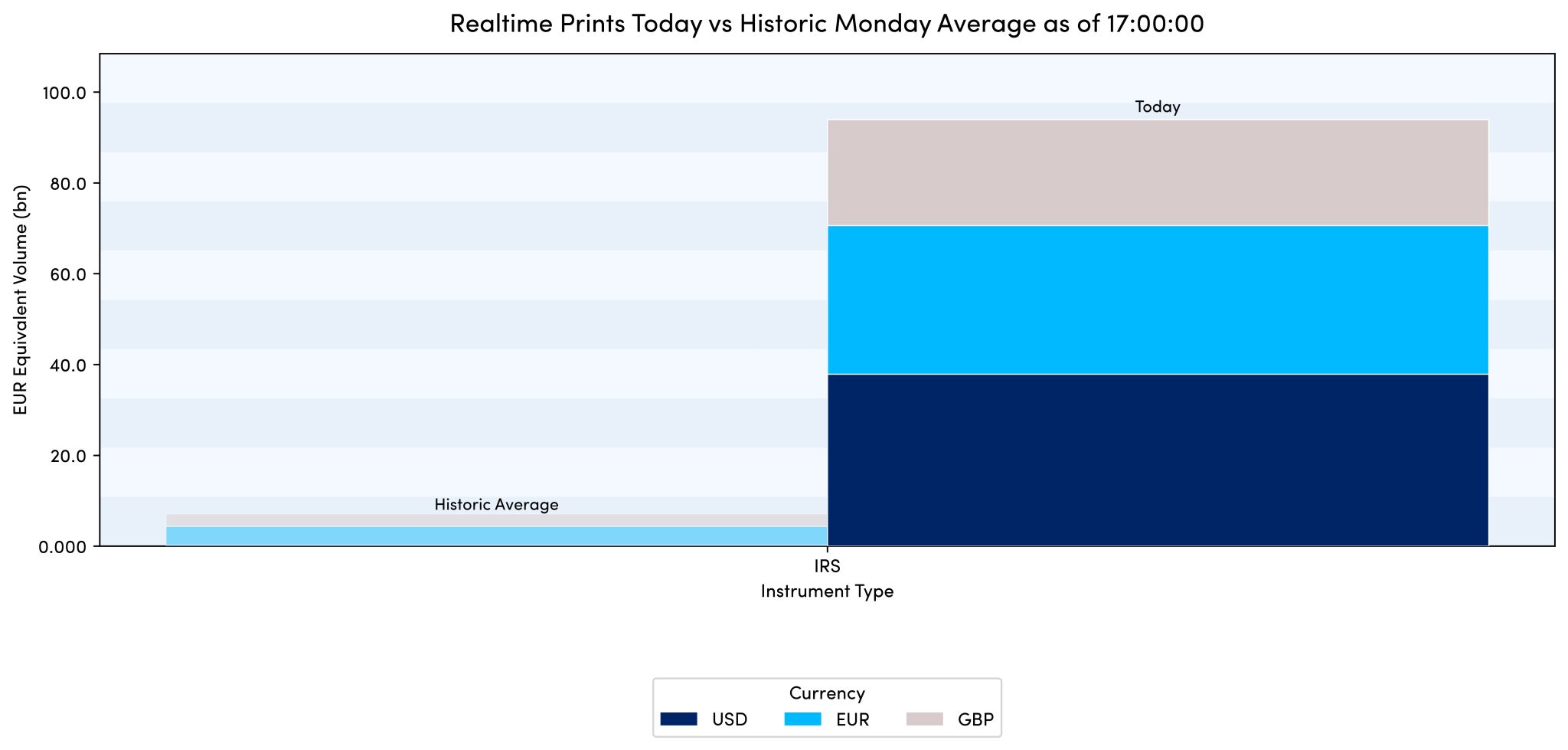

3. All asset classes by end of day

Chart 4, 5, 6 show that real-time reported volumes for bonds, IRS, and CDS have all increased substantially, indicating that the new reporting rules are successfully adopted by market participants across the board.

Across OTC derivative trades, there is an increase of more than 7x the typical Monday volume reported, in real-time, with Debt Securities - both sovereign and non-sovereign - showing around a 5x increase.

We will provide some further insights as the week goes on. If you would like to find out more about the new regime, please get in touch with us.

.png)

.png)

.png)