It is likely that many (perhaps most) readers will be aware that the 23rd football World Cup kicks off on 11th June, and it feels too good an opportunity for us to pass up to look at all 48 participating countries and see the volumes reported under MiFID.

We go through each group and look at the year-to-date MiFID volumes for each country (in EUR equivalent volume).

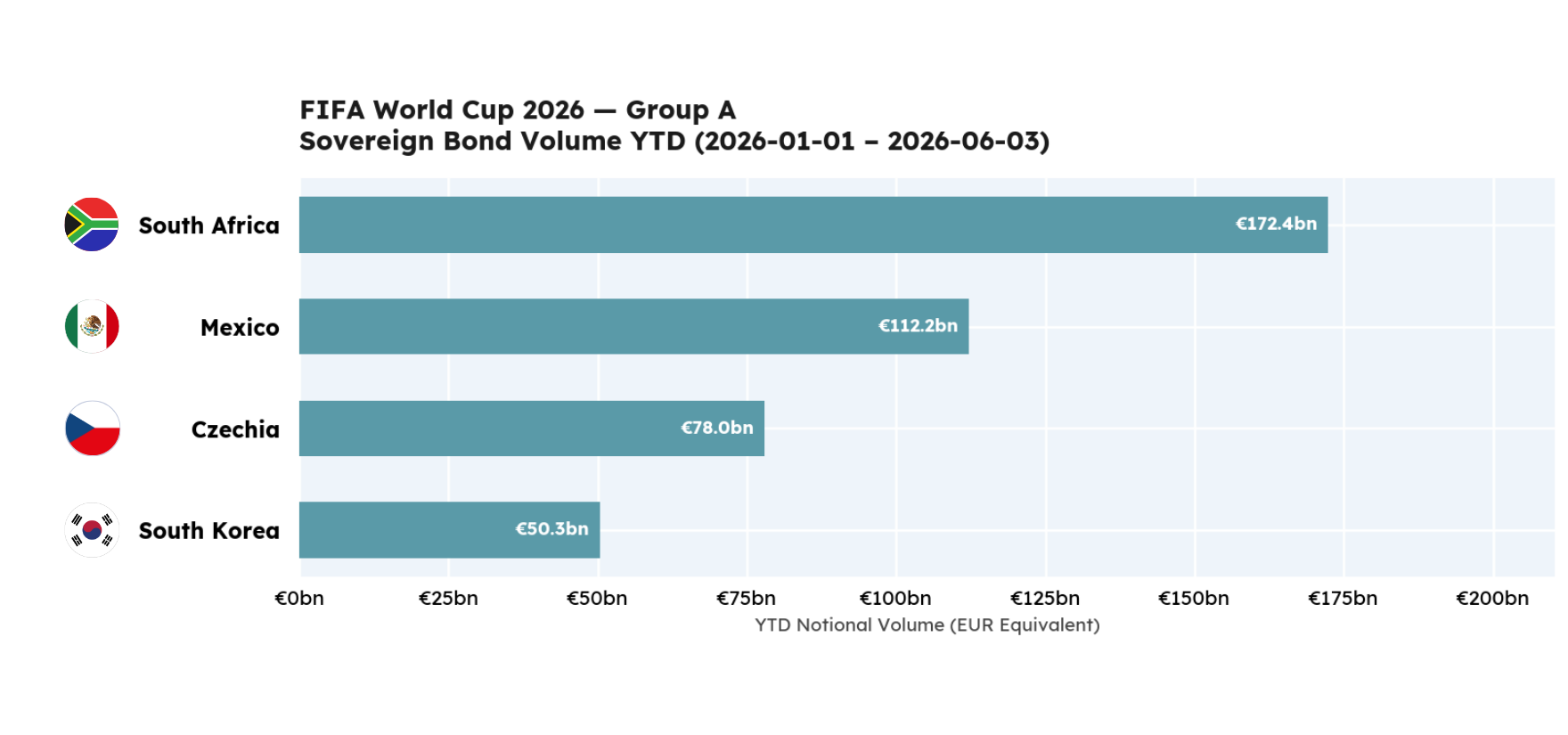

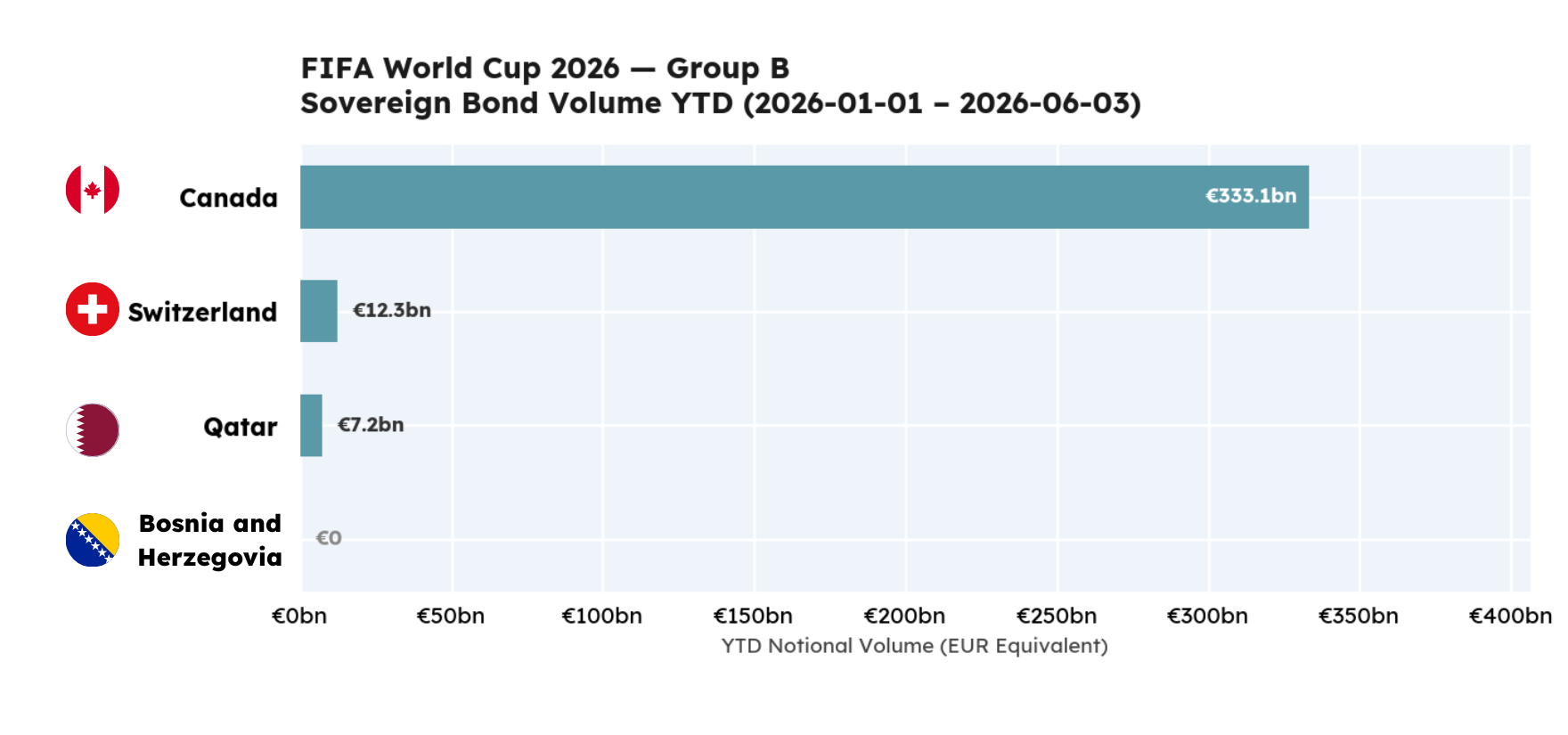

Both Group A and B have clear front runners, with South Africa and Canada comfortably out in front.

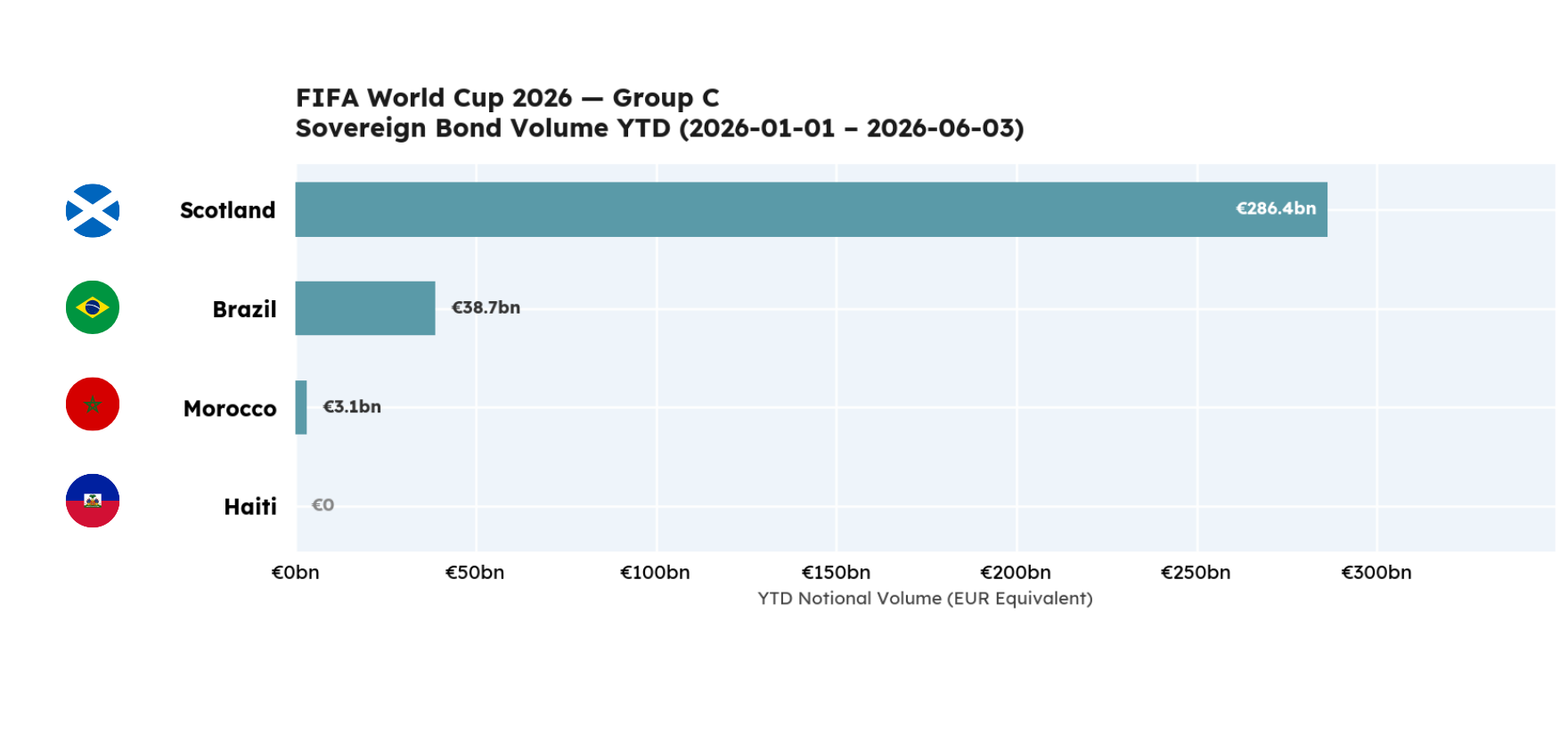

Moving onto Group C, we perhaps find our first surprise, with Scotland racing past Brazil (for the avoidance of doubt, we proportionally split UK debt by GDP).

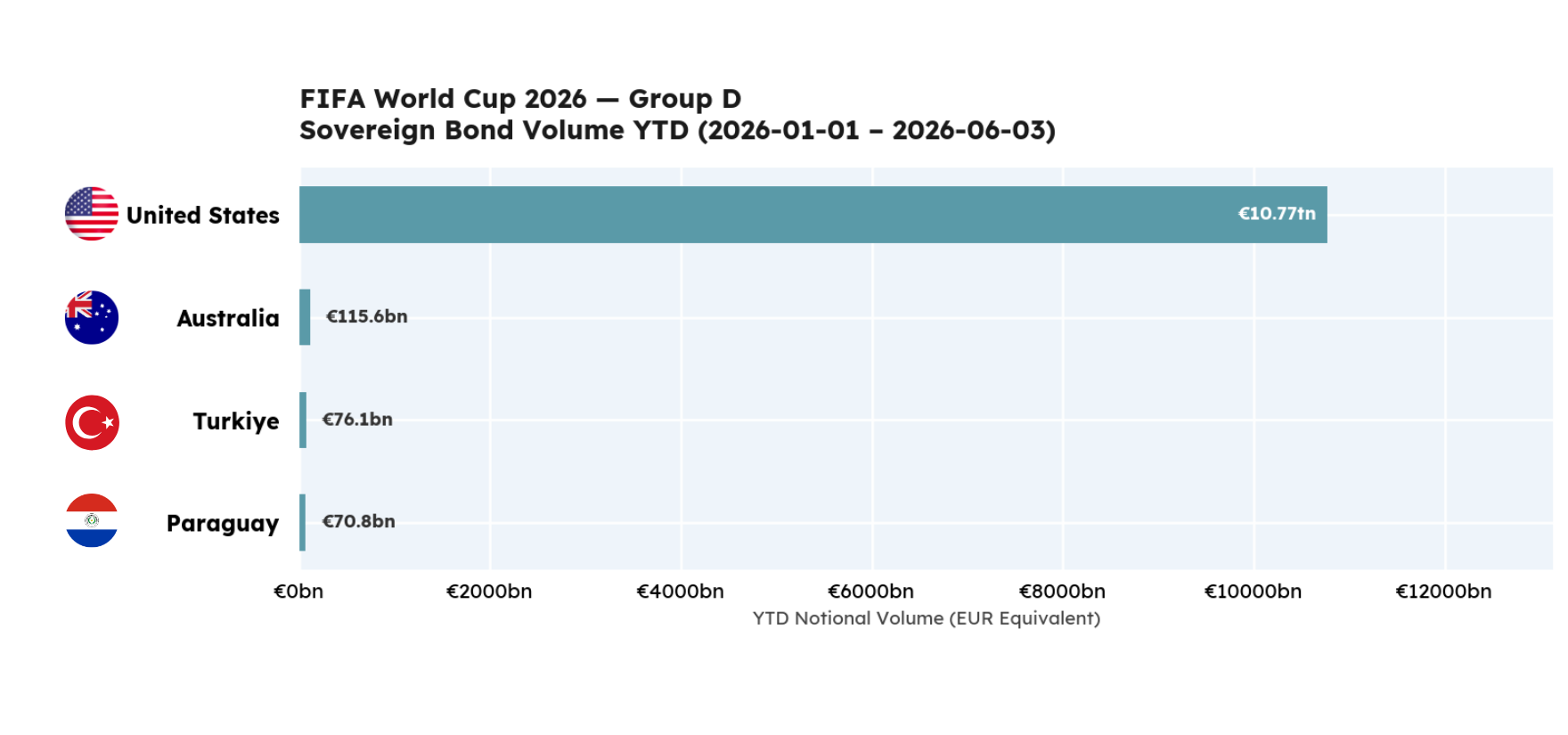

Probably the least surprising result so far, the US has the most actively traded yield curve in the world (and MiFID reporting only captures a subset of this). It is also worth mentioning that AUD denominated debt is also widely traded outside of Europe (and hence not fully captured).

“There is no question that the US is knocking this out of the park. The games are on our home turf, we have this in the bag.”

Elizabeth Brooks Callaghan

Senior Advisor

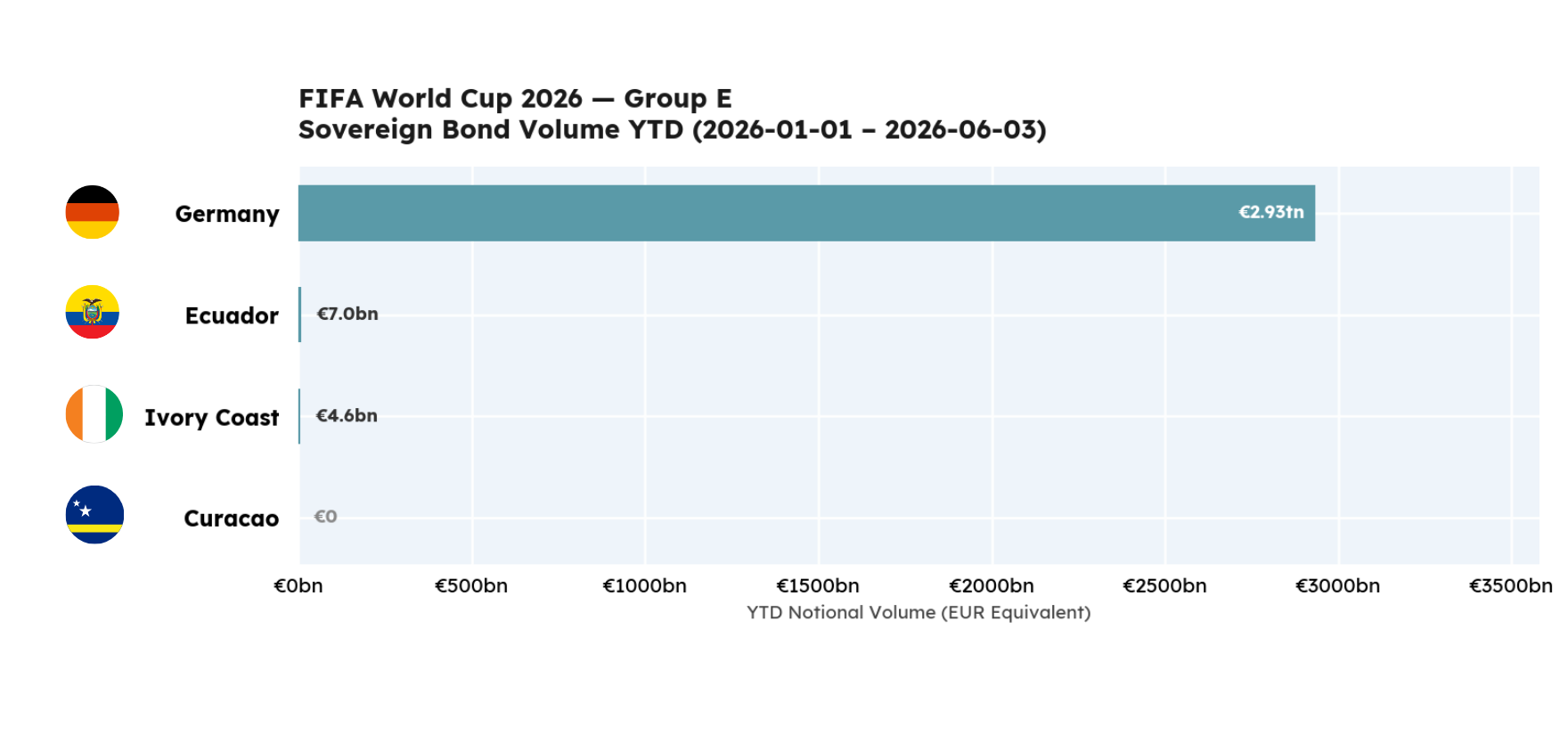

This group presented us with a bit of a challenge, as we could not find any activity on Curacao (the smallest country to reach the World Cup) and up against Germany. It is clear who is dominating this pool, both in the footballing and debt markets sense.

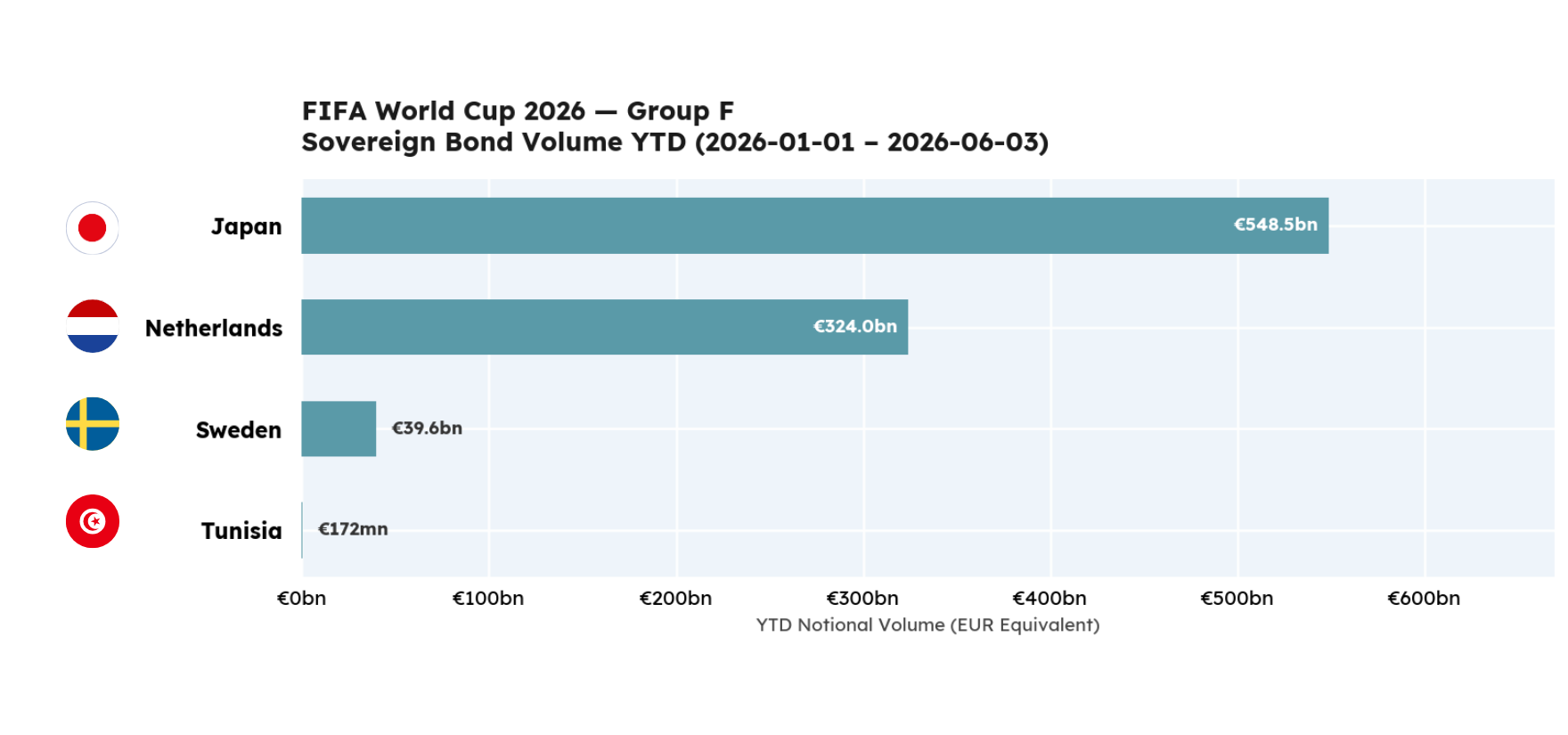

“I note Japan is currently ahead, albeit not by much. Hup Holland Hup! The Netherlands are favourites, we will bring it back.”

Pom Burie

Chief Financial Officer

This group is arguably slightly unexpected, not because Japan is not a highly active issuer, but because a lot of JGB debt trades domestically, rather than in Europe. Therefore, as with the US, even though the numbers are not small, there is additional volume that is not accounted for here.

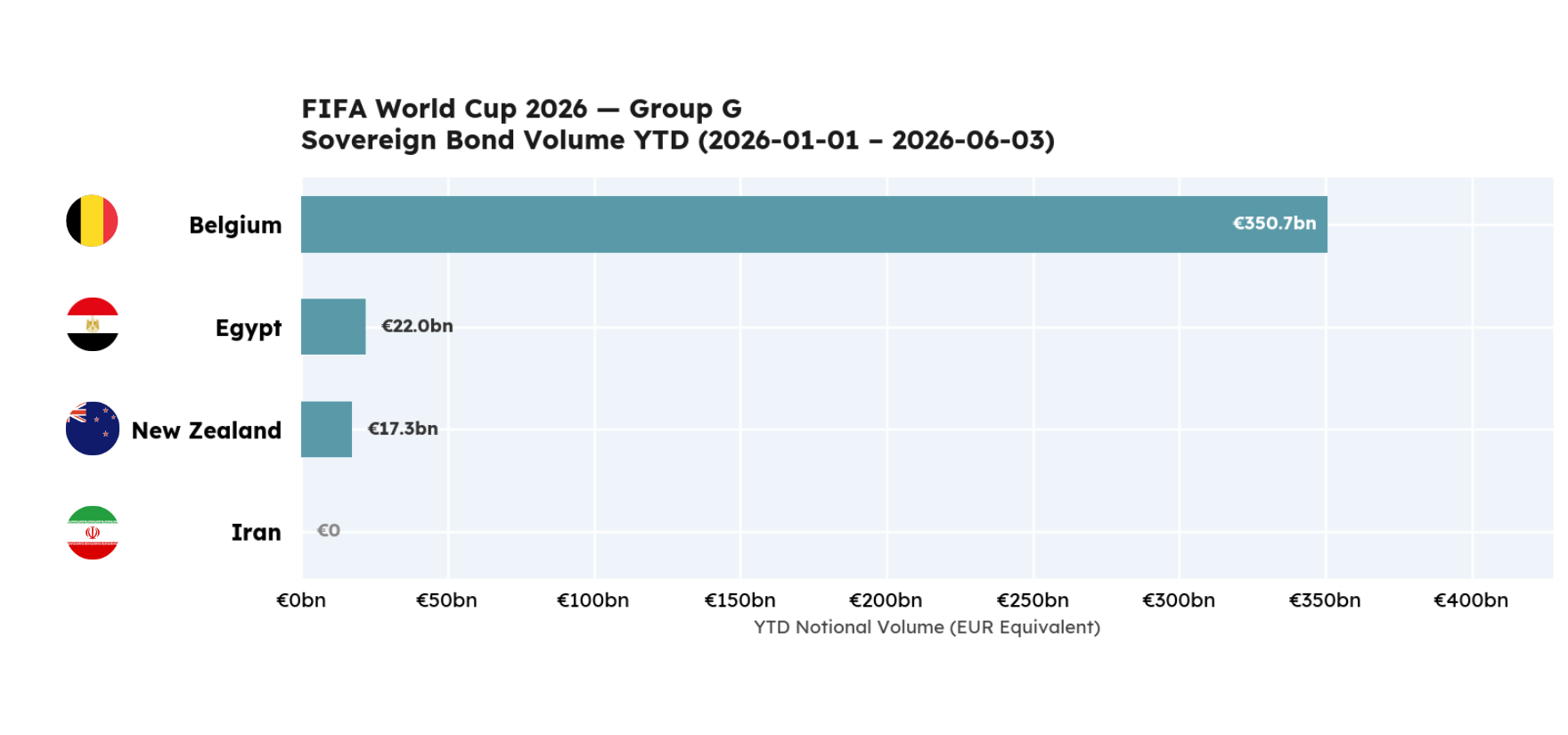

“There is no surprise Belgium have taken the lead here. Allez les Diables!”

Vincent Grandjean

Founder and CEO

“Whilst Belgium may lead currently, we finished our last World Cup undefeated... I back New Zealand as underdogs!”

Helena Roughton

Product Manager, Regulatory Focus

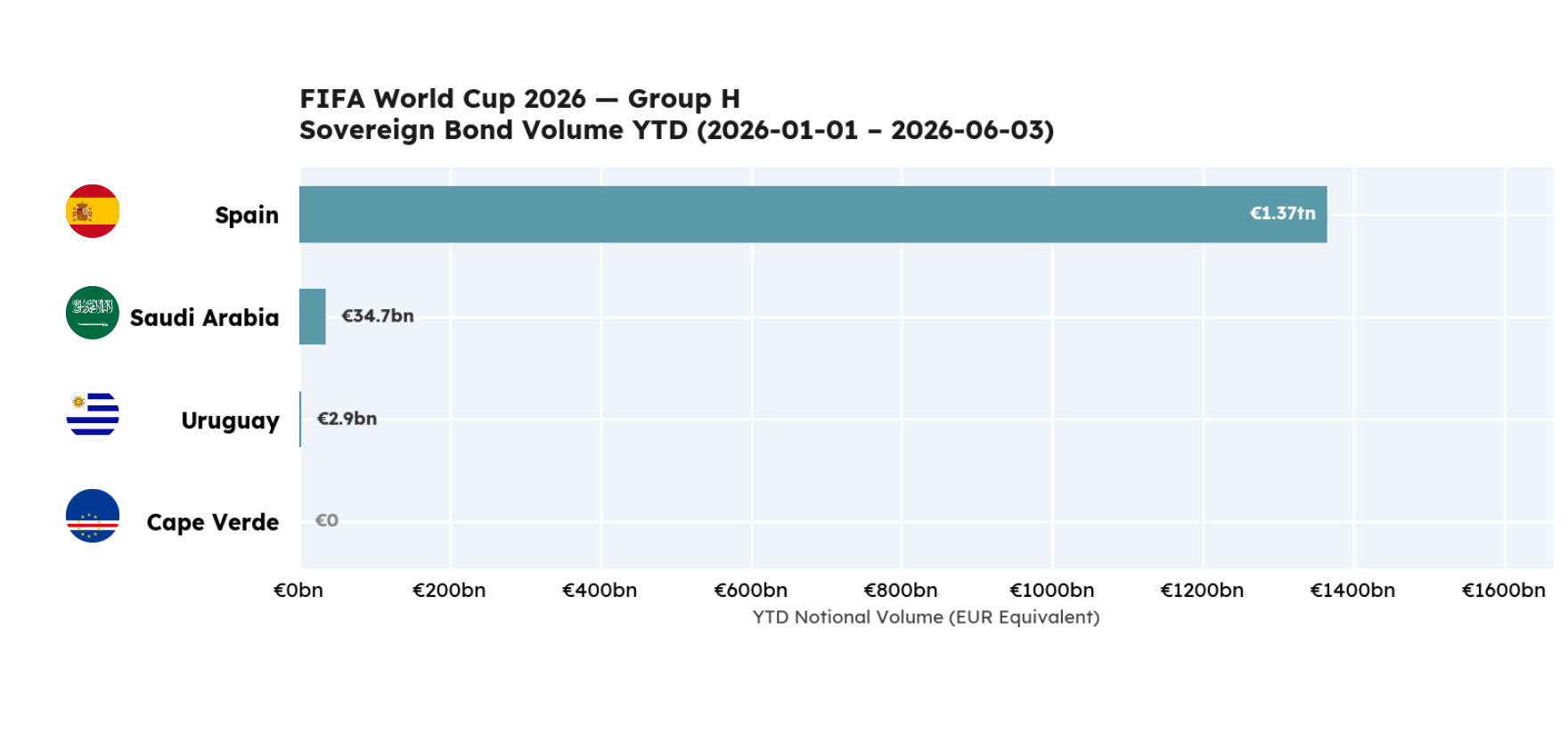

Spain has the pedigree as a former winner. However Saudi Arabia, the giant killers (beating eventual winners Argentina last time round), could cause an upset. Football aside, Spain is a highly active issuer and sees substantial secondary market flow across the curve. Saudi Arabia, meanwhile are one of the more active issuers in the Middle East and have a developed USD curve now, with billions of secondary activity reported under MiFID.

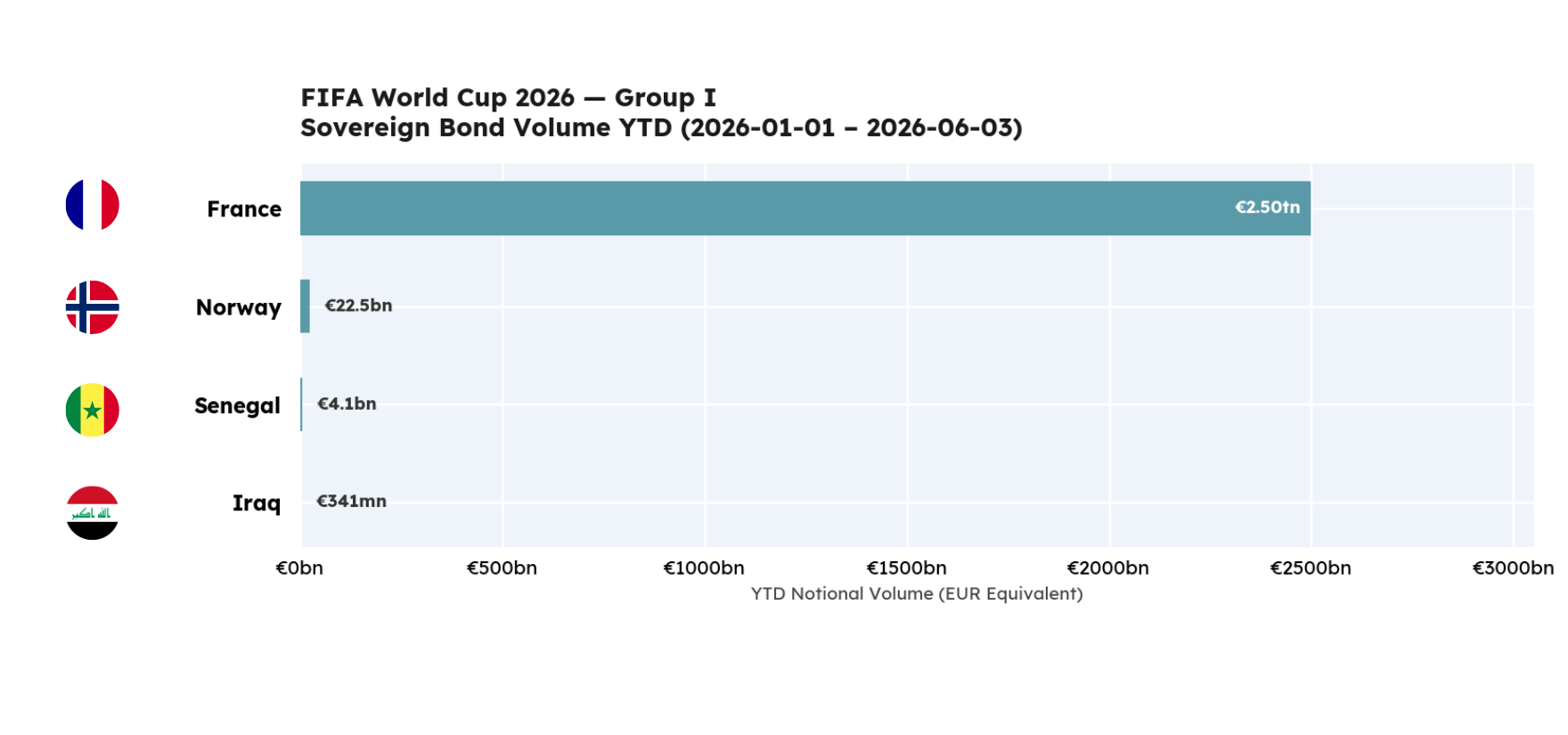

“In the Group of Death, France have torn well ahead of other top teams. Allez les Bleus!”

Caroline Wohleber

Senior Sales

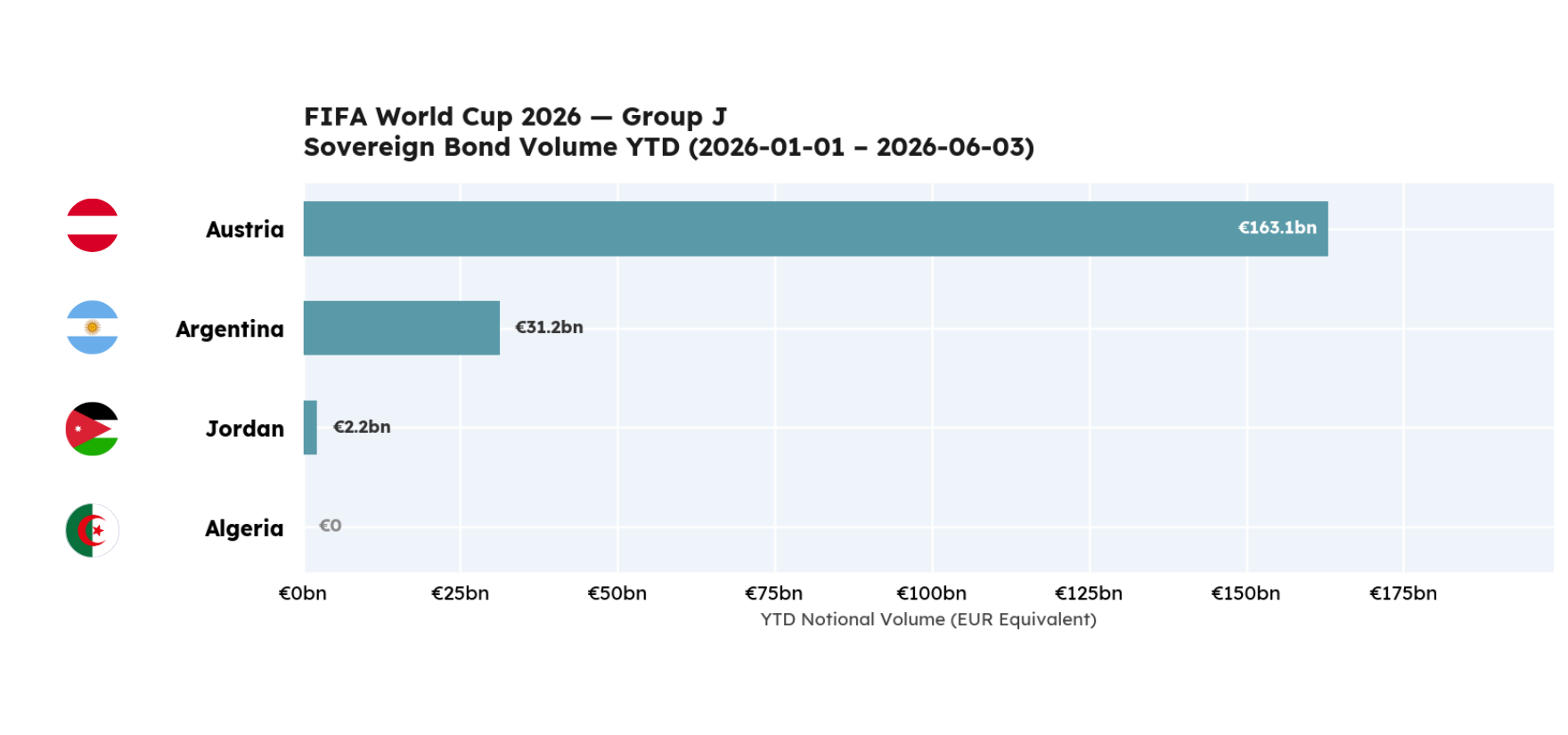

The reigning champions have fallen! Austria have surprisingly taken the lead, but with Messi on the pitch, will they keep it?

That may well seem an unlikely event (in footballing terms), but in the debt markets Austria has far higher volumes reported under MiFID. We should highlight, however, that Argentina (despite a chequered history when it comes to defaulting) does commonly issue debt not only in Argentinian Pesos, but also USD, meaning a lot of activity takes place within the Americas.

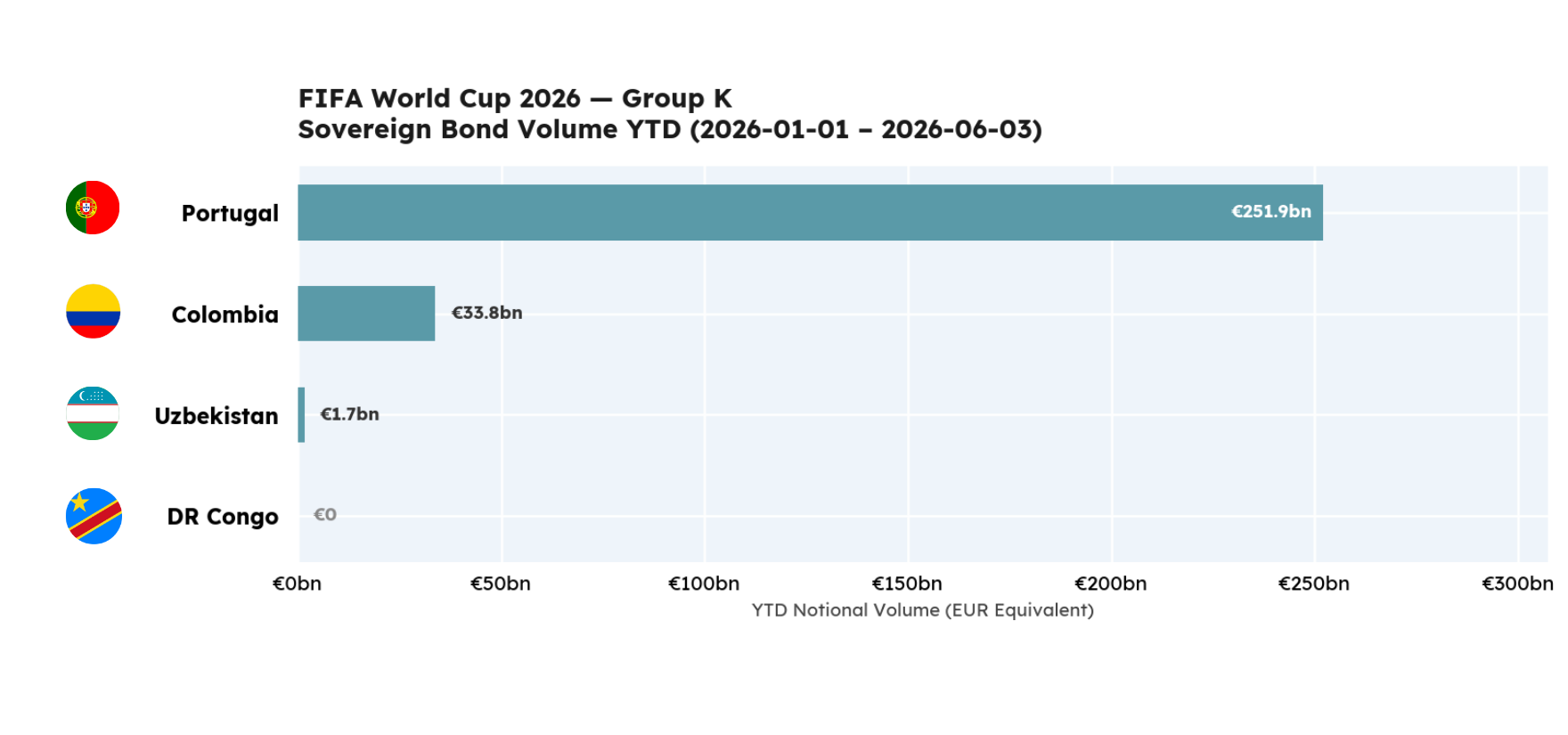

“Portugal's time is now! The GOAT in his final dance and the best midfield we've had in our history, controlling every game. No more dreaming, the cup is coming home. Siuuuuuu!”

Bruno Grifo

Developer

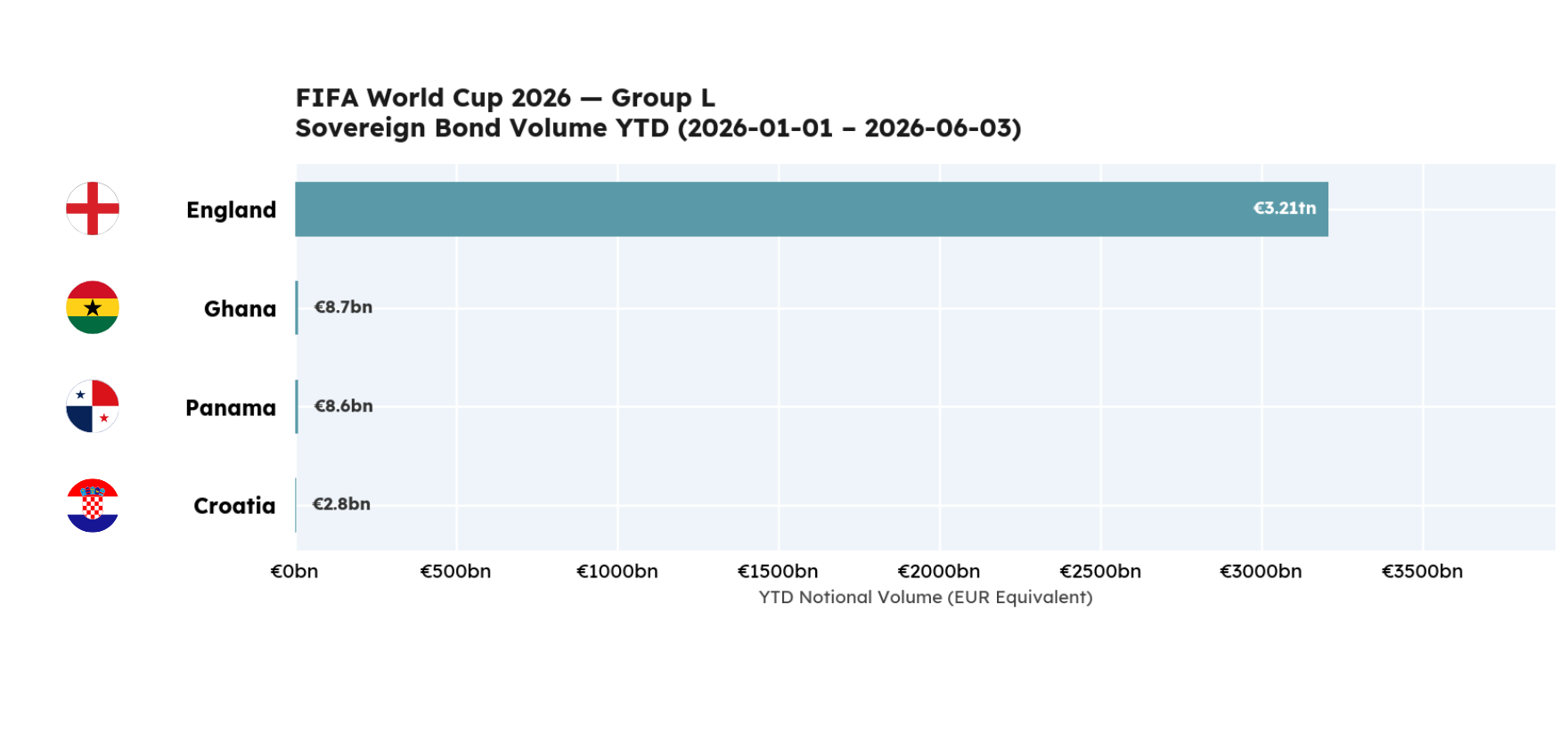

“England is obviously tearing ahead in their pool and I have full confidence that we will bring it home.”

Charlie Gibson

Chief Commercial Officer

The volume shown against England is proportionally adjusted by UK GDP and at least from a debt perspective England look set to storm into the next round!

%20(4).png)

%20(2).png)